AI樂觀情緒與出口規定鬆綁提振科技股;關稅不確定性持續,整體市場漲跌互見

Joe Lu, CFA 2025年5月14日 美東時間

市場概況

美國股市週三呈現漲跌互見的局面,科技類股,特別是半導體股,推動那斯達克綜合指數連續第六個交易日上漲,而整體市場的標普500指數漲幅較為溫和,道瓊工業平均指數則微幅收低。市場主導題材仍是圍繞AI領域的樂觀情緒和特定公司消息,與持續存在且影響深遠的貿易關稅及其最終經濟衝擊的不確定性之間的相互作用。儘管本週稍早美中關稅暫緩帶來了顯著的寬慰,但市場目前正努力應對許多仍在進行中的貿易談判,以及關稅格局具體細節仍不確定的現實。

標普500指數微升+0.13%,而道瓊工業平均指數則下跌-0.23%。以科技股為主的 那斯達克綜合指數表現明顯突出,上漲+0.60%。代表小型股的 羅素2000指數下跌-0.89%。此種分歧突顯出市場日益依賴少數領漲股,主要集中在科技和AI領域。

輝達(NVIDIA)(+4.16%)再次成為正面情緒的關鍵推手,延續近期的飆升態勢,並正式抹去2025年以來的所有跌幅。此波漲勢受惠於其近期與沙烏地阿拉伯達成的AI晶片協議所帶來的持續熱情,並進一步得到美國商務部已啟動撤銷拜登時代「人工智慧擴散規則 (AI Diffusion Rule)」的消息支撐,這可能放寬部分晶片出口的限制。超微(AMD)等同業晶片股亦反彈。然而,關稅的更廣泛影響持續蒙上陰影。蘋果主要合作夥伴暨輝達伺服器製造商-鴻海,儘管受AI需求推動季度利潤飆升,卻因關稅不確定性而下調了全年展望。同樣地,索尼(Sony)發布了令人失望的財測,預計美國關稅將帶來7億美元的負面影響。美國鷹(American Eagle)等零售商也因「總體經濟不確定性」而撤回財測,突顯了企業在當前貿易政策環境下,進行規劃時所面臨的挑戰。這些全球性企業的謹慎態度,與特定科技股的樂觀情緒形成重要的對比。

重點摘要

美股週三收盤漲跌互見;在半導體類股反彈的帶動下,那斯達克綜合指數(+0.60%)連續第六個交易日上漲,標普500指數(+0.13%)微幅收高,道瓊指數(-0.23%)則下滑。

- 輝達(+4.16%)持續強勁漲勢,抹去今年以來所有跌幅,受惠於與沙烏地阿拉伯達成的重大AI晶片協議以及美國可能放寬晶片出口限制的消息。

- 儘管科技股反彈且近期美中關稅暫緩,但整體關稅不確定性依然是顯著的不利因素,鴻海和索尼等公司的保守展望以及零售商撤回財測即為證明。

- 分析顯示投資存續期間仍極為不利,顯示市場深層的謹慎情緒,而消費者信心和通膨指標今日走強,呈現複雜的經濟景象。

- 投資者關注焦點:判斷當前由科技和AI驅動的樂觀情緒能否克服持續的關稅不確定性,並轉化為更廣泛、可持續的市場力道,尤其是在「迷因式」投機活動再現之際。

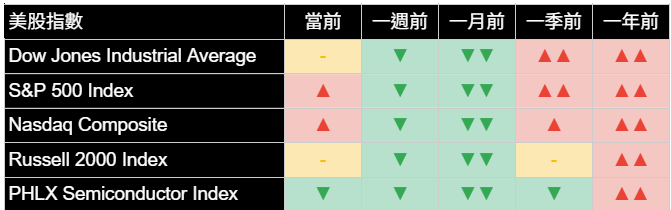

主要市場指數

主要市場指數週三收盤漲跌互見,科技股表現突出。那斯達克綜合指數上漲+0.60%,連續第六個交易日上漲。標普500指數微幅收高+0.13%。相較之下,道瓊工業平均指數下跌-0.23%,代表小型股的 羅素2000指數則下跌-0.89%。此表現突顯當前市場依賴少數科技領漲股,而更對廣泛的領域則信心不足。

費城半導體指數上漲+0.33%,相較於其部分大型成分股,漲幅較為溫和,顯示即使在反彈的晶片領域也存在一定的選擇性。儘管近期價格走勢正面,但對該族群的底層分析普遍持續顯示,在較長的時間區間內其狀況仍屬不利。

從分析角度來看,根據我們的指標顯示,今日漲跌互見的表現,使得標普500指數和那斯達克綜合指數的近期市場特性仍維持有利,建立在近期的改善基礎之上。然而,道瓊工業平均指數和羅素2000指數則雙雙維持中度不利的評估。此種分歧表明,儘管特定領域表現強勢,但整體市場尚未確認潛在狀況的廣泛、可持續的改善。

美國前十大公司

美國大型企業週三表現好壞參半,部分科技股(尤其是與AI相關者)漲勢強勁,而其他股票則呈現溫和波動或下跌。

觀察個股當日表現:輝達(NVIDIA Corp)持續其亮眼表現,上漲+4.16%,並抹去今年以來的跌幅。Alphabet Inc A股(Alphabet Inc Class A)亦錄得強勁漲幅,上漲+3.66%。特斯拉(Tesla Inc)上揚+4.07%。微軟(Microsoft Corp)上漲+0.85%。Meta Platforms Inc上漲+0.51%。相較之下,蘋果(Apple Inc)下跌-0.28%。亞馬遜(Amazon.com Inc)亦下跌-0.53%。博通(Broadcom Inc)下跌-0.13%。摩根大通(JPMorgan Chase & Co)上漲+1.00%,而波克夏海瑟威B股(Berkshire Hathaway Inc Class B)則下跌-1.66%。

從底層分析面來看,這些領先科技企業中數檔的近期市場特性仍為有利或中性。分析顯示,微軟(Microsoft Corp)、亞馬遜(Amazon.com Inc)、Meta Platforms Inc和特斯拉(Tesla Inc)的狀況有利。博通(Broadcom Inc)亦維持其有利狀態。輝達(NVIDIA Corp)的狀況現為中性。然而,蘋果(Apple Inc)的狀況仍極為不利,Alphabet Inc A股(Alphabet Inc Class A)則為中度不利。摩根大通(JPMorgan Chase & Co)維持其有利評估,而波克夏海瑟威B股(Berkshire Hathaway Inc Class B)則維持中性。特定AI相關個股的持續強勢與其他部分大型股潛在的謹慎訊號形成對比。

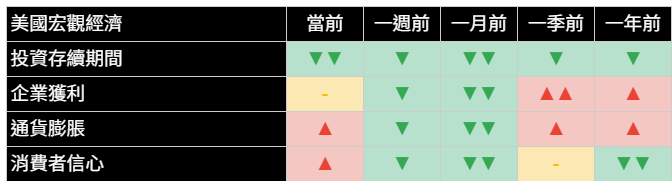

經濟指標

今日市場活動並無重大的美國經濟數據發布,使投資者焦點得以持續放在進行中的關稅政策討論、企業財報以及對未來數據的預期上。市場仍處於「眼見為憑」的階段,企業獲利需要趨於穩定,財測指引也需要恢復。對潛在「關稅引發的衰退」或「僵固性通膨 (Sticky Inflation)」的擔憂,依然是許多市場參與者首要考量的因素,影響著風險偏好。昨日公布的四月份CPI數據年增2.3%,暫時緩解對當前通膨的擔憂恐懼,但在不斷變化的關稅格局下,其長期影響仍在評估中。

我們整套經濟指標今日展現了情勢的變化。分析顯示,投資存續期間的訊號仍極為不利,未見改善,反映出市場對長期經濟風險持續且強烈的規避。企業獲利前景維持中性。值得注意的是,消費者信心和通膨訊號今日雙雙走強,分別從中性/中度正向轉為中度正向和強勁正向。這表明市場衍生的指標今日正捕捉到消費者韌性增強和通膨預期上升的訊號,此為一關鍵發展。這種極為不利的投資存續期間與走強的消費者信心和通膨並存的組合,呈現出一種複雜且可能處於循環後期的動態,值得投資者密切關注。

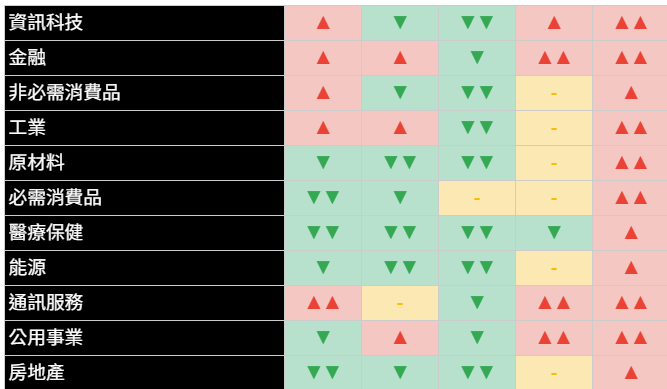

類股概況

標普500指數各類股週三表現漲跌互見,反映出主要指數走勢分歧以及市場當前的選擇性。科技股和部分成長型領域表現突出,而防禦型和其他週期性類股則表現落後。

資訊科技類股(+0.71%)是領漲類股之一,受惠於輝達等半導體股的強勢以及其他大型科技股的上漲。非必需消費品類股(+0.39%)亦上揚,特斯拉是重要的貢獻者。通訊服務類股(+0.52%)亦錄得上漲,儘管內部表現分歧。能源類股(-0.61%)和金融類股(-0.27%)小幅下跌。工業類股(-0.48%)和原物料類股(-0.96%)亦收低。防禦型類股大多疲弱:醫療保健類股(-2.35%)表現最差,延續近期的弱勢,根據部分報導,現已成為今年以來表現最差的標普500子產業。必需消費品類股(-0.54%)和公用事業類股(-0.44%)亦下跌。房地產類股(-0.99%)跌幅顯著。

從分析角度來看,根據我們的指標,資訊科技、金融和非必需消費品類股的近期特性維持有利。工業類股維持有利評估。然而,包括能源、原物料、醫療保健、必需消費品、公用事業和房地產在內的多數其他類股,其狀況仍為不利或中性,通訊服務類股亦屬有利。這強化了漲勢範圍狹窄的論點,領漲力道集中在特定的成長型市場區塊,而更廣泛的市場參與仍然猶豫。

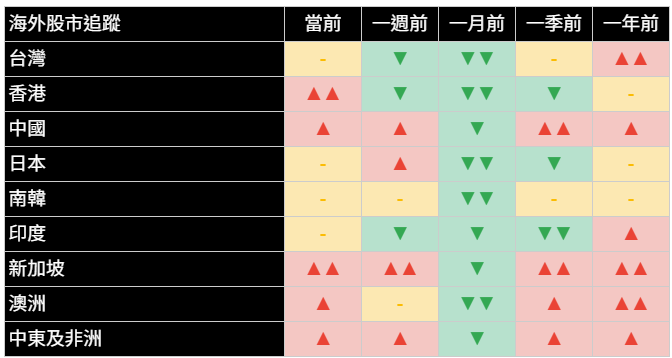

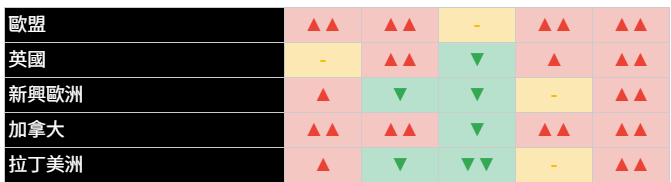

國際市場

國際市場週三表現好壞參半,全球投資者持續權衡近期美中關稅緊張局勢降溫的影響,以及持續存在的全球經濟不確定性和各國特定因素。美元走強,當日上漲+0.22%。

已開發市場大多收低:歐洲股市下跌-0.23%,日本股市下跌-1.11%。美元走強可能構成不利因素。分析持續顯示,從較長的時間區間來看,這些地區的潛在特性普遍為正,但它們對全球風險偏好的轉變仍然敏感。

新興市場亦呈現不同結果:新興亞洲市場上漲+0.91%,而印度下跌-0.07%,拉丁美洲則收平(0.00%)。中國股市強勁上漲+1.65%。此種分歧突顯了對國際配置採取細緻化策略的重要性。

其他資產

週三其他資產類別的活動反映出謹慎基調,債券出現需求,美元走強,大宗商品則大多下跌。

固定收益方面,由於股市在科技股方面展現出一些韌性,美國 公債價格 大多下跌(殖利率上揚)。短期公債價格 下跌-0.07%,中期公債價格 下跌-0.41%,長期公債價格 亦下滑-0.66%。整體美國綜合債券價格 下跌-0.29%。這表明前一日的避險需求略有消退。

大宗商品表現普遍為負。WTI原油 下跌-1.24%。黃金價格 亦顯著下跌,跌幅達-2.10%,受美元走強以及在近期上漲後可能出現部分獲利了結的壓力。基本金屬(+1.02%) 則有所斬獲。農產品 下跌-0.55%。美元指數 走強,上漲+0.22%。在數位資產方面,比特幣價格 下跌-1.48%。

若要持續接收我們針對美國經濟、股市和產業的深度分析與洞見,請訂閱我們的電子報。

歡迎將此分析分享給可能覺得有價值的人士。

立即加入《Joe’s 華爾街脈動》LINE@官方帳號,獲得最新專欄資訊(點此加入)

關於《Joe’s 華爾街脈動》

鉅亨網特別邀請到擁有逾 22 年美國投資圈資歷、CFA 認證的機構操盤人 Joseph Lu 擔任專欄主筆。 Joe 為台裔美國人,曾管理超過百億美元規模的基金資產,並為總資產高達數千億美元的多家頂級金融機構提供資產配置優化建議。 Joe 目前帶領著由美國頂尖大學教授與博士組成的精英團隊,透過獨家開發的 "趨勢脈動 TrendFolios® 指標",為台灣投資人深度解析全球市場脈動,提供美股市場第一手專業觀點,協助投資人掌握先機。

Nasdaq Notches Sixth Straight Gain as Nvidia, Chips Lead Tech Rally Amid Tariff Crosscurrents

Tech Surges on AI Optimism and Export Rule Easing; Broader Market Mixed as Tariff Uncertainty Persists

Joe Lu, CFA May 14, 2025

EXECUTIVE SUMMARY

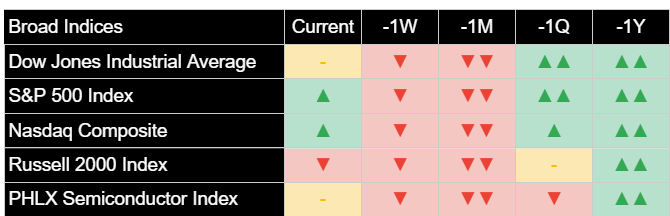

U.S. stocks finished mixed Wednesday; the Nasdaq Composite (+0.60%) extended its winning streak to six days, driven by a rally in semiconductor stocks, while the S&P 500 (+0.13%) edged higher and the Dow (-0.23%) slipped.

- Nvidia (+4.16%) continued its strong advance, erasing its year-to-date losses, fueled by major AI chip deals with Saudi Arabia and potential easing of U.S. chip export curbs.

- Despite the tech rally and recent U.S.-China tariff pause, broader tariff uncertainty remains a significant headwind, evidenced by cautious outlooks from companies like Foxconn and Sony, and retailers withdrawing guidance.

- Analysis shows Investment Duration remains pronouncedly unfavorable, signaling deep-seated caution, while Consumer Strength and Inflation indicators firmed today, presenting a complex economic picture.

- Key for investors: discerning whether the current tech and AI-driven optimism can overcome persistent tariff uncertainties and translate into broader, sustainable market strength, especially as "meme-like" speculative activity reappears.

MARKET OVERVIEW

U.S. equity markets presented a mixed picture on Wednesday, with the technology sector, particularly semiconductors, driving the Nasdaq Composite to its sixth consecutive day of gains, while the broader S&P 500 posted a more modest advance and the Dow Jones Industrial Average finished slightly lower. The dominant theme remains the interplay between optimism surrounding the AI sector and specific company news, versus the persistent and overarching uncertainty related to trade tariffs and their ultimate economic impact. While the U.S.-China tariff pause earlier in the week provided significant relief, the market is now grappling with the reality that many trade negotiations are ongoing, and the specifics of the tariff landscape remain fluid.

The S&P 500 Index edged up +0.13%, while the Dow Jones Industrial Average declined -0.23%. The tech-heavy Nasdaq Composite Index was the clear outperformer, gaining +0.60%. Small-capitalization stocks, represented by the Russell 2000 Index, fell -0.89%. This divergence underscores a market increasingly reliant on a narrow set of leaders, primarily within the technology and AI space.

NVIDIA (+4.16%) was a key driver of positive sentiment again, extending its recent surge and officially erasing all its losses for 2025. This rally was fueled by ongoing enthusiasm from its recent AI chip deals with Saudi Arabia and further supported by news the U.S. Department of Commerce has initiated the rescission of the Biden-era "AI Diffusion rule," potentially easing some chip export curbs. Peer chip stocks like AMD also rallied. However, the broader impact of tariffs continues to cast a shadow. Foxconn, a major Apple partner and Nvidia server maker, posted a surge in quarterly profit driven by AI demand but notably cut its full-year outlook, citing tariff uncertainty. Similarly, Sony issued a disappointing forecast, expecting a $700 million negative impact from U.S. tariffs. Retailers like American Eagle also withdrew guidance due to "macro uncertainty," highlighting the challenges businesses face in planning amidst the current trade policy environment. This caution from globally exposed companies serves as a critical counterpoint to the exuberance in select tech names.

BROAD MARKET INDICES

Broad market indices finished mixed on Wednesday, with technology outperforming. The Nasdaq Composite Index gained +0.60%, marking its sixth straight day of gains. The S&P 500 Index edged higher by +0.13%. In contrast, the Dow Jones Industrial Average fell -0.23%, and the Russell 2000 Index, representing small-cap stocks, declined -0.89%. This performance highlights the current market's dependence on a narrow band of technology leaders, while broader segments exhibit less conviction.

The PHLX Semiconductor Index gained +0.33%, a more modest advance compared to some of its large-cap components, suggesting some selectivity even within the rallying chip space. Despite recent positive price action, underlying analysis for this group generally continues to indicate unfavorable conditions over extended timeframes.

From an analytical perspective, today's mixed performance saw the near-term market character for the S&P 500 and Nasdaq Composite remain favorable according to our indicators, building on recent improvements. However, the Dow Jones Industrial Average and the Russell 2000 Index both maintained their moderately unfavorable assessments. This divergence suggests that while specific segments are showing strength, a broad-based, sustainable improvement in underlying market conditions has yet to be confirmed across the entire market.

TOP 10 U.S. COMPANIES

Performance among the largest U.S. companies was mixed on Wednesday, with strong gains in some tech names, particularly those linked to AI, while others saw modest moves or declines.

Looking at individual stock performance for the day: NVIDIA Corp continued its impressive run, gaining +4.16% and erasing its year-to-date losses. Alphabet Inc Class A also posted a strong gain, rising +3.66%. Tesla Inc advanced +4.07%. Microsoft Corp added +0.85%. Meta Platforms Inc gained +0.51%. In contrast, Apple Inc declined -0.28%. Amazon.com Inc also fell -0.53%. Broadcom Inc fell -0.13%. JPMorgan Chase & Co gained +1.00%, while Berkshire Hathaway Inc Class B fell -1.66%.

Interpreting the underlying analytical picture, the near-term market character for several of these leading tech companies remains favorable or neutral. Analysis shows favorable conditions for Microsoft Corp, Amazon.com Inc, Meta Platforms Inc, and Tesla Inc. Broadcom Inc maintained its favorable state. NVIDIA Corp's condition is now neutral. However, conditions for Apple Inc remained pronouncedly unfavorable and Alphabet Inc Class A moderately unfavorable. JPMorgan Chase & Co maintained its favorable assessment, while Berkshire Hathaway Inc Class B stayed neutral. The continued strength in select AI-related names contrasts with the underlying caution signals for some other mega-caps.

ECONOMIC INDICATORS

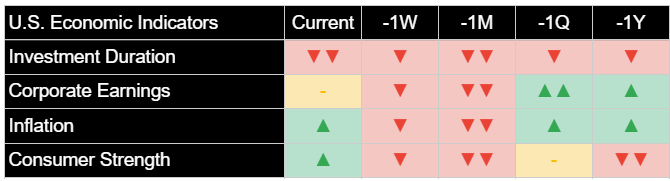

Today's market activity occurred without major U.S. economic data releases, allowing investor focus to remain on ongoing tariff policy discussions, corporate earnings, and anticipation of future data. The narrative of a "show me" market, where earnings need to stabilize and guidance needs to return, persists. Concerns about a potential "tariff-induced recession" or "sticky inflation" remain top of mind for many market participants, influencing risk appetite. The April CPI data released yesterday, showing a 2.3% year-over-year increase, provided some temporary relief from immediate inflation fears, but its longer-term implications in a shifting tariff landscape are still being assessed.

Our suite of economic indicators today presented a picture of evolving conditions. Analysis indicated the Investment Duration signal remained pronouncedly unfavorable, showing no improvement and reflecting a persistent, strong aversion to longer-term economic risk. The Corporate Earnings outlook remained neutral. Notably, both the Consumer Strength and Inflation signals firmed today, moving from neutral/moderately positive to moderately positive and strongly positive respectively. This suggests that market-derived indicators are picking up on increased consumer resilience and rising inflation expectations today, which is a critical development. This combination of pronouncedly unfavorable Investment Duration alongside firming Consumer Strength and Inflation presents a complex, potentially late-cycle dynamic that warrants close investor attention.

SECTOR OVERVIEW

Sector performance within the S&P 500 was mixed on Wednesday, reflecting the divergent paths of the major indices and the market's current selectivity. Technology and some growth areas outperformed, while defensives and other cyclicals lagged.

Information Technology (+0.71%) was a leading sector, driven by the strength in semiconductor stocks like Nvidia and gains in other large-cap tech. Consumer Discretionary (+0.39%) also advanced, with Tesla being a significant contributor. Communication Services (+0.52%) posted gains as well, though internal divergence persisted. Energy (-0.61%) and Financials (-0.27%) saw modest declines. Industrials (-0.48%) and Materials (-0.96%) also finished lower. Defensive sectors were mostly weak: Healthcare (-2.35%) was the worst performer, continuing its recent underperformance and now the worst-performing S&P 500 subsector year-to-date according to some reports. Consumer Staples (-0.54%) and Utilities (-0.44%) also declined. Real Estate (-0.99%) posted a notable loss.

From an analytical perspective, the near-term character for Information Technology, Financials, and Consumer Discretionary remained favorable based on our analysis. Industrials maintained a favorable assessment. However, conditions for most other sectors, including Energy, Materials, Healthcare, Consumer Staples, Utilities, and Real Estate, remained unfavorable or neutral, with Communication Services also favorable. This reinforces the theme of a narrow rally, with leadership concentrated in specific growth segments while broader market participation remains tentative.

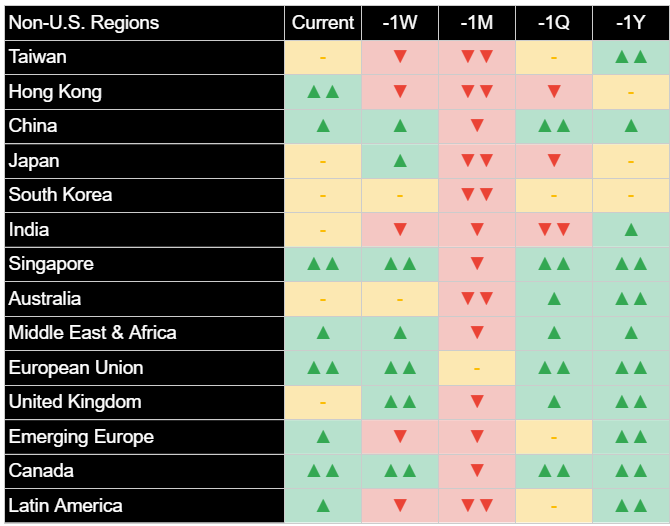

INTERNATIONAL MARKETS

International markets displayed mixed performance on Wednesday, as global investors continued to weigh the implications of the recent U.S.-China tariff de-escalation against ongoing global economic uncertainties and country-specific factors. The U.S. Dollar strengthened, rising +0.22% for the day.

Developed markets were mostly lower: European equities fell -0.23% and Japanese equities declined -1.11%. The stronger dollar likely posed a headwind. Analysis continues to indicate generally positive underlying characteristics for these regions over longer horizons, but they remain susceptible to shifts in global risk appetite.

Emerging markets also showed varied results: Emerging Markets Asia gained +0.91%, while India fell -0.07%, and Latin America finished flat (0.00%). Chinese equities posted a strong gain of +1.65%. This divergence highlights the importance of a granular approach to international allocations.

OTHER ASSETS

Activity across other asset classes on Wednesday reflected a cautious tone, with bonds seeing some demand, the dollar firming, and commodities mostly lower.

In fixed income, U.S. Treasury prices were mostly lower (yields higher) as the equity market showed some resilience in tech. Short-term Treasury prices fell -0.07%, Intermediate Treasury prices dropped -0.41%, and Long-term Treasury prices also slid -0.66%. Broad U.S. Aggregate Bond prices decreased -0.29%. This indicates a slight unwind of the previous day's safe-haven demand.

Commodity performance was predominantly negative. WTI Crude Oil fell -1.24%. Gold prices also declined significantly, losing -2.10%, pressured by the firmer dollar and perhaps some profit-taking after recent gains. Base Metals (+1.02%) managed a gain. Agricultural Commodities fell -0.55%. The US Dollar Index strengthened, rising +0.22%. In digital assets, Bitcoin prices declined -1.48%.

To continue receiving our in-depth analysis and insights focused on the U.S. economy, stocks and sectors, please subscribe to our newsletter.

Consider sharing this analysis with others who might find it valuable.

Join the official LINE account of "Joe’s Wall Street Pulse" now to receive the latest column updates (click here to join)