•

【Joe’s華爾街脈動】關稅隱憂撼動市場,亮麗財報季蒙上陰影

貿易緊張局勢再度引發投資者謹慎,產業前景轉變

Joe 盧, CFA 2025年5月23日 美東時間

重點摘要

- 由於美國總統宣布可能對歐盟進口商品和蘋果iPhone徵收新關稅,此番言論重新引發了對國際貿易摩擦的擔憂,全球市場普遍下跌。此一發展蓋過了基本上正面的企業財報季,並在陣亡將士紀念日(Memorial Day)週末前夕帶來了謹慎的氣氛。投資者的關鍵問題是,這些重新浮現的貿易擔憂究竟是短暫的,抑或預示著對經濟成長和企業獲利能力更為持久的不利因素。

- 包括標普500指數和道瓊工業指數在內的美國股價指數雙雙回落,其中標普500指數的趨勢惡化至負面。此一轉變,加上其他主要市場區塊持續不利的前景,顯示投資者的憂慮情緒升高。

- 以蘋果公司為首的美國主要科技公司,因新進口關稅的前景而面臨下行壓力。這導致資訊科技類股的趨勢轉為負面。相較之下,公用事業和必需消費品等傳統防禦型類股則展現相對強勢,其趨勢轉為正面。

- 美國企業獲利前景的評估轉為負面,而消費者信心的展望則趨緩至中性。儘管近期基本面具韌性,這些變化反映了市場擔憂關稅可能壓縮利潤空間並抑制經濟活動。

- 國際市場方面,歐洲股市因關稅消息而下跌。然而,亞洲市場則呈現一定的活力,部分受到中國政策寬鬆的影響。黃金價格上漲,可能反映了市場尋求避險資產的趨勢。

市場觀點

週五,美方針對歐盟進口商品和蘋果iPhone提出新的關稅威脅,引發市場明顯不安,蓋過了財報季後期本應帶來的利多氣氛。這種持續的地緣政治貿易風險,引發了市場的避險情緒,導致股市回落,因參與者評估潛在的影響。儘管企業基本面表現穩健,市場的反應凸顯了其對貿易政策的持續敏感性。這帶出了一個問題:如果這些政策全面實施,是否將嚴重衝擊既有的供應鏈和國際貿易。

此不確定性亦影響其他資產類別。隨著市場對潛在貿易中斷及其更廣泛經濟影響的擔憂加劇,債券殖利率下降,10年期公債殖利率跌至4.51%。此走勢延續了近期從較高殖利率水平逆轉的趨勢。美元兌主要國際貨幣走弱。海外市場方面,歐洲股市直接受到關稅威脅的影響而下跌,而亞洲市場則受惠於中國的新貨幣寬鬆措施。大宗商品市場表現分歧;據報導,儘管預期OPEC+可能增加供應,原油價格仍上漲,為全球經濟前景增添了另一個變數。儘管財報季基本上表現正面,有相當比例的標普500指數成分股公司業績超出預期,但關稅疑慮的再起為投資者帶來了新的審慎因素。

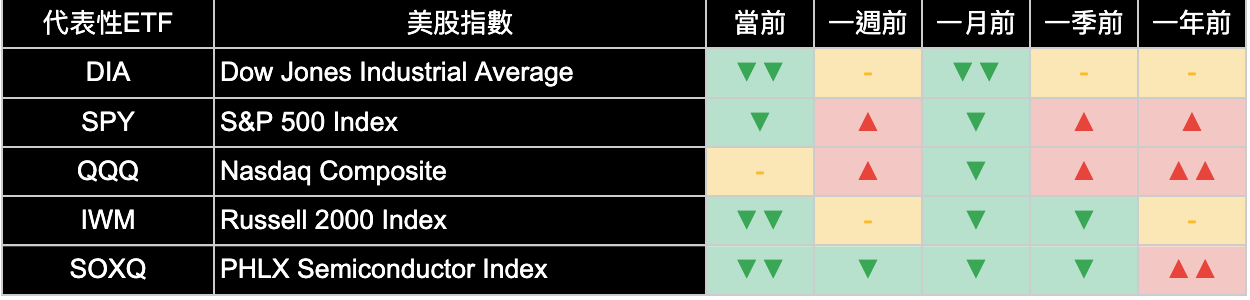

主要指數

由於對關稅的擔憂再起,美國主要股價指數週五下跌。標普500指數下跌(-0.68%),其趨勢從先前中性轉為負面。道瓊工業指數下跌(-0.59%),維持其深度負面趨勢。那斯達克綜合指數回落(-0.93%),但維持中性展望,而反映小型公司表現的羅素2000指數下跌(-0.31%),並持續呈現強烈負面趨勢。費城半導體指數在這些基準指數中跌幅最大,下跌(-1.46%),亦維持強烈負面趨勢。

關稅議題的再起構成了相當大的阻力,可能蓋過原本強勁的財報季。標普500指數趨勢轉為負面,加上其他幾個關鍵指數持續疲弱的評估,顯示投資者日益謹慎。在此背景下,市場開始思考近期漲勢的持久性,以及這些貿易擔憂是否可能擴大為整體經濟放緩,進而影響各類股的企業獲利能力。

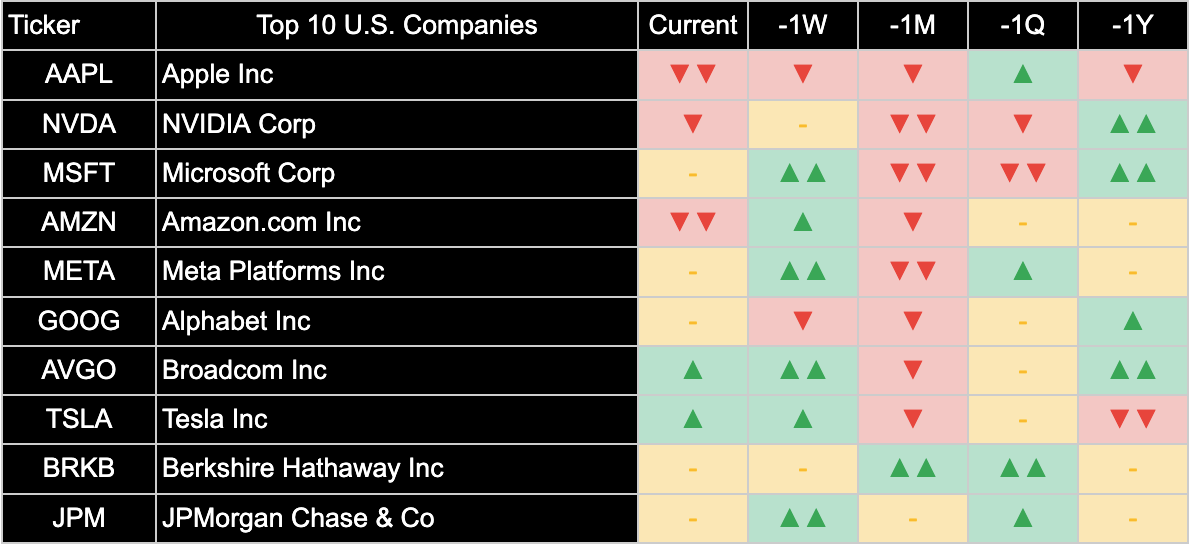

美國前十大企業

數家美國龍頭企業股價於週五下跌。在iPhone可能面臨進口關稅的消息被特別提及後,蘋果(Apple Inc.)股價出現顯著單日跌幅(-3.02%)。輝達(NVIDIA Corp)亦下跌(-1.16%),亞馬遜(Amazon.com Inc.)則下跌(-1.04%)。微軟(Microsoft Corp)(-1.03%)、Meta Platforms (Meta Platforms Inc)(-1.49%)、Alphabet (Alphabet Inc)(-1.40%)、博通(Broadcom Inc)(-0.79%)及特斯拉(Tesla Inc)(-0.50%)亦收低。反之,摩根大通(JPMorgan Chase & Co)錄得小幅上漲(+0.02%),而波克夏海瑟威(Berkshire Hathaway Inc)則近乎持平(-0.02%)。蘋果(Apple Inc.)和亞馬遜(Amazon.com Inc.)的趨勢仍維持深度負面。輝達(NVIDIA Corp)的趨勢轉為負面。微軟(Microsoft Corp)、Meta Platforms (Meta Platforms Inc)、Alphabet (Alphabet Inc)、特斯拉(Tesla Inc)、波克夏海瑟威(Berkshire Hathaway Inc)及摩根大通(JPMorgan Chase & Co)均維持中性展望。博通(Broadcom Inc.)持續呈現正面趨勢,儘管其上升動能似乎有所趨緩。

蘋果公司被直接點名納入關稅討論,突顯了即使是美國最大的企業也難以倖免於地緣政治貿易緊張局勢的影響。對投資者而言,輝達公司趨勢轉負以及蘋果公司和亞馬遜持續低迷的評估,顯示科技和以消費者為重心的巨頭尤其敏感。此情勢需要密切關注關稅威脅的進展及其對企業盈餘的潛在衝擊,特別是對於擁有大量國際業務的公司。

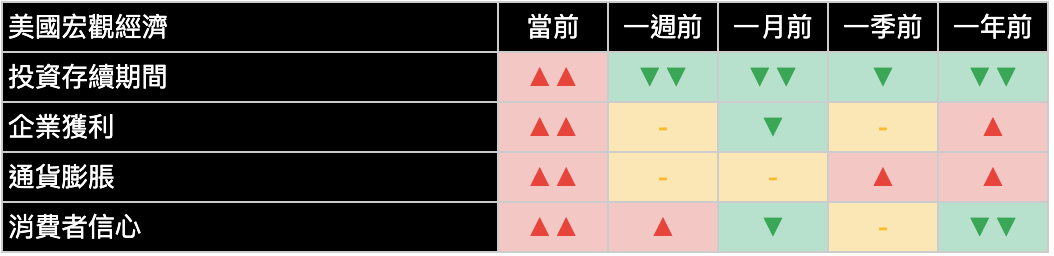

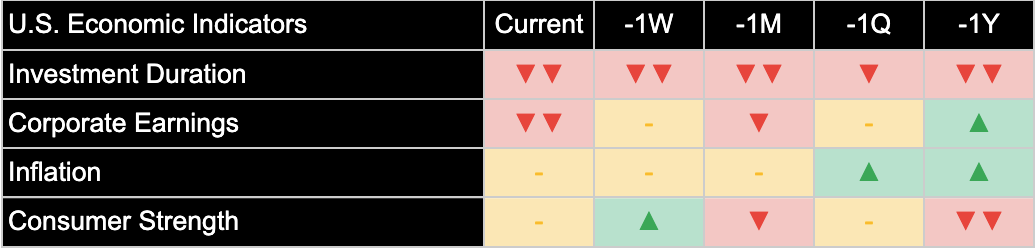

美國經濟指標

整體經濟信心轉趨審慎。投資存續期間的評估仍維持深度負面,顯示對利率敏感性較高的長期資產而言,環境依然充滿挑戰。值得注意的是,儘管近期財報季表現強勁,企業獲利的前景已轉為負面,與市場擔憂新關稅可能壓縮利潤空間的看法一致。對通膨的看法則維持中性評估。消費者信心亦呈現中性立場,較先前正面的評估有所轉弱,暗示以消費者為驅動的經濟活動可能出現趨緩。

企業獲利展望轉為負面是一項關鍵的發展,意味著若新關稅實施,近期強勁的獲利成長可能面臨阻力。此情況加上投資存續期間持續不利的前景以及消費者信心的趨緩,顯示經濟不確定性升高。投資者應考量這些因素將如何影響整體經濟成長,以及若貿易摩擦導致投入成本上升,目前對通膨的中性立場是否能夠持續。

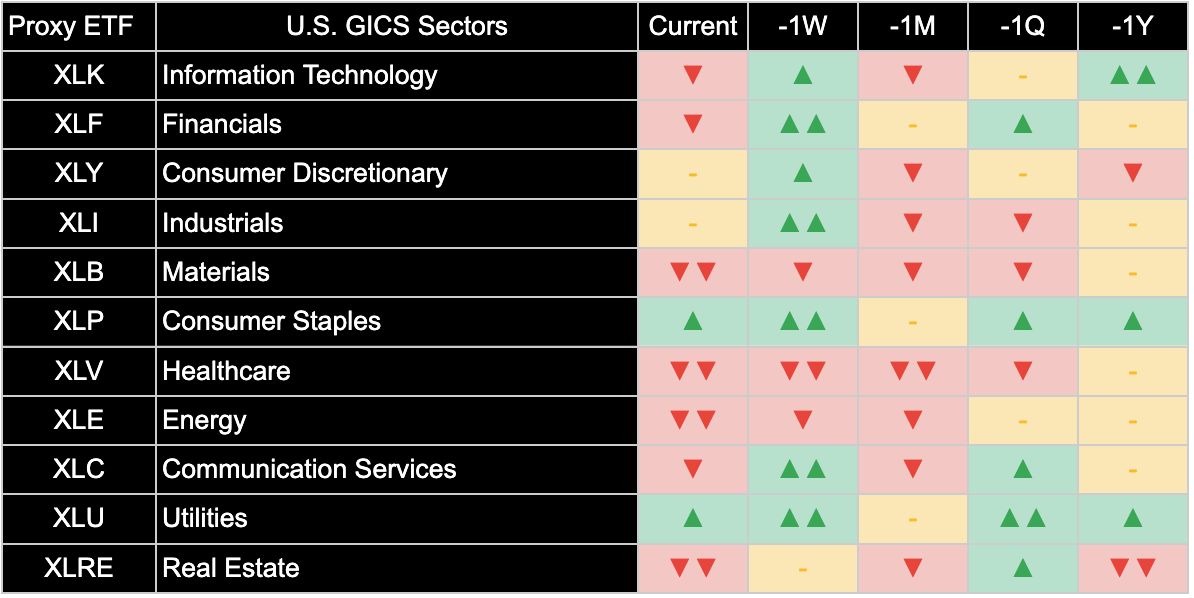

類股焦點

美國多數類股週五回檔。資訊科技類股單日價格下跌(-1.10%),其趨勢轉為負面。金融類股下跌(-0.36%),其趨勢亦從先前強勁正面轉為負面。非必需消費品類股下跌(-0.90%),其趨勢降溫至中性。工業類股(-0.33%)的趨勢亦從強勁正面轉為中性。原物料類股下跌(-0.20%),維持深度負面趨勢。反之,必需消費品類股上漲(+0.37%),其趨勢轉為正面,而公用事業類股上漲(+1.20%),其趨勢亦轉為正面。醫療保健類股(-0.16%)維持深度負面趨勢。儘管處於深度負面趨勢,能源類股(+0.32%)仍小幅上漲。通訊服務類股下跌(-0.46%),其趨勢轉為負面。不動產類股近乎持平(+0.02%),其趨勢維持深度負面。

資訊科技和金融等關鍵類股的趨勢轉為負面,加上非必需消費品和工業類股趨勢降溫,顯示關稅消息對市場造成廣泛衝擊。必需消費品和公用事業等傳統防禦型類股趨勢改善,可能意味著資金正流向被視為安全的資產。此一分歧引發市場對主導類股結構的重新思考,也使投資人開始評估,若貿易緊張局勢升級,是否應採取更具防禦性的資產部署。

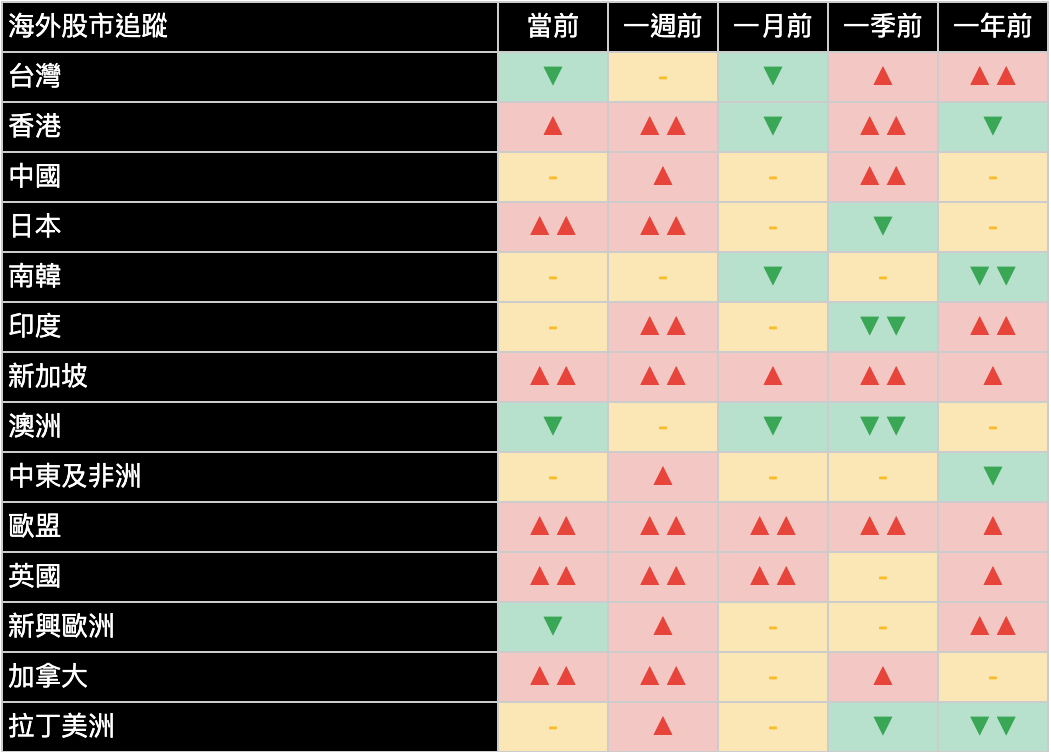

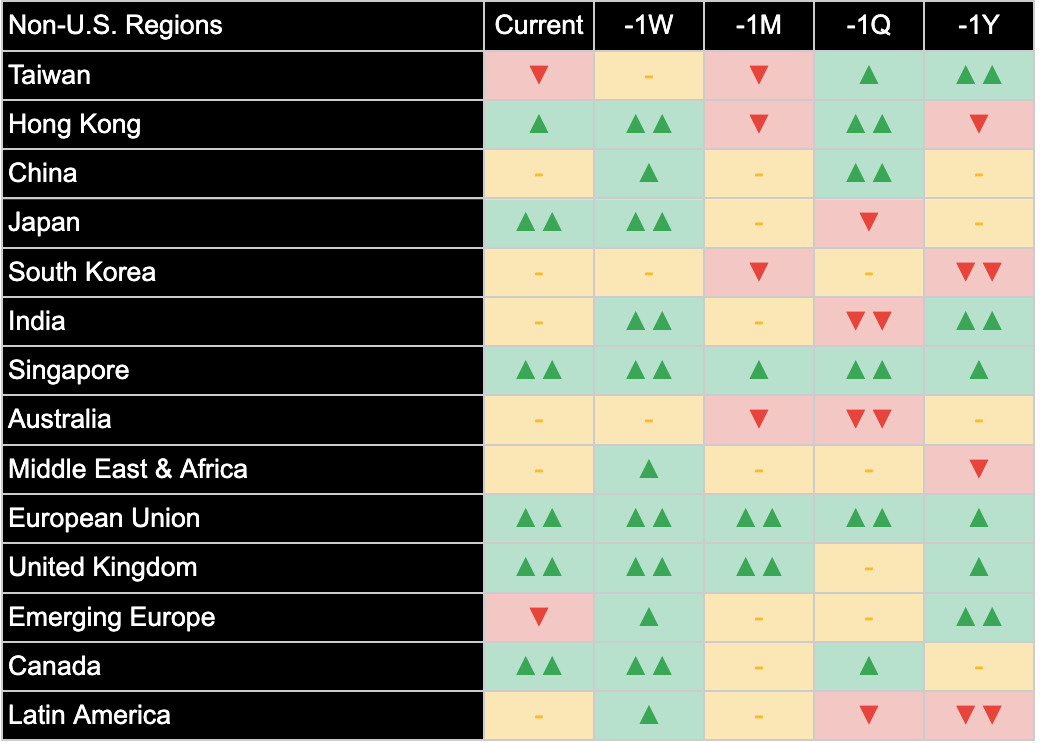

國際市場

國際市場表現各異。在美國發表關稅聲明後,歐盟市場走低,該地區代表指數下跌(-0.16%);儘管如此,歐盟仍維持強勁正面趨勢。另一方面,日本市場上漲(+0.91%),其趨勢增強至強勁正面。在新的貨幣寬鬆措施支持下,中國市場亦小幅走高(+0.05%),不過其趨勢趨緩至中性。印度市場上漲(+1.47%),其趨勢改善至中性。其他地區方面,台灣市場趨勢轉為負面。香港市場維持正面趨勢。南韓市場趨勢改善至中性。新加坡市場持續其強勁正面趨勢。澳洲市場維持中性。中東及非洲地區的趨勢降溫至中性。新興歐洲市場趨勢轉為負面。加拿大市場維持其強勁正面趨勢,而拉丁美洲市場的趨勢則趨緩至中性。

美國關稅的言論對歐洲市場的直接衝擊,突顯了全球經濟的相互關聯性。反之,日本市場趨勢轉強以及中國的政策放寬,則展現了不同的區域動態。在此背景下,國際資產配置策略需更加細緻,審慎考量各區域的脆弱性以及對貿易發展的政策回應能力。

其他資產

黃金表現亮眼,單日價格上漲(+2.19%);其趨勢維持正面。然而,比特幣則下跌(-2.21%),儘管其趨勢仍維持強勁正面。原油價格上漲(+1.27%);其趨勢仍維持深度負面。固定收益方面,1-3年期公債小幅上漲(+0.06%),其趨勢維持中性。7-10年期公債亦上漲(+0.29%),不過其趨勢為負面。20年以上期公債微幅上漲(+0.17%),但其趨勢仍維持深度負面。工業金屬上漲(+0.70%),趨勢為中性,而農產品則下跌(-0.95%),趨勢亦為中性。

黃金的上漲突顯了其在市場承壓時的傳統避險角色。比特幣的下跌,儘管長期趨勢正面,顯示其易受整體市場衝擊的影響。公債價格的正面走勢反映了資金流向優質資產,與殖利率下降的趨勢一致。大宗商品價格的波動將受到密切關注,以判斷貿易緊張局勢可能如何影響全球供需。

保持聯繫並分享見解:

若您覺得本文有幫助,請點讚支持。

- 請將此電子報轉發給可能認為有價值的同事和朋友。

- 訂閱即可直接在您的收件匣中接收此分析。

- 在社群媒體上關注我們以獲取更多更新。

本電子報僅供參考之用,並不構成任何投資建議或買賣任何證券或資產類別的推薦。文中所述觀點為作者截至發布日期之意見,並可能隨時更改,恕不另行通知。所提供資訊乃基於從相信屬可靠來源獲取之數據,但其準確性、完整性及及時性不獲保證。過往表現並非未來業績的指標。投資涉及風險,包括可能損失本金。讀者在做出任何投資決策前,應諮詢其自身的財務顧問。作者及相關實體可能持有本文所討論之資產或資產類別的部位。

立即加入《Joe’s 華爾街脈動》LINE@官方帳號,獲得最新專欄資訊(點此加入)

關於《Joe’s 華爾街脈動》

鉅亨網特別邀請到擁有逾 22 年美國投資圈資歷、CFA 認證的機構操盤人 Joseph Lu 擔任專欄主筆。

Joe 為台裔美國人,曾管理超過百億美元規模的基金資產,並為總資產高達數千億美元的多家頂級金融機構提供資產配置優化建議。

Joe 目前帶領著由美國頂尖大學教授與博士組成的精英團隊,透過獨家開發的 "趨勢脈動 TrendFolios® 指標",為台灣投資人深度解析全球市場脈動,提供美股市場第一手專業觀點,協助投資人掌握先機。

Tariff Tremors Shake Markets, Clouding Strong Earnings Season

Renewed Trade Tensions Spark Investor Caution, Shifting Sector Outlooks

By Joe 盧, CFA As of May 23, 2025

EXECUTIVE SUMMARY

- Global markets broadly declined as presidential pronouncements regarding potential new tariffs on European Union imports and Apple iPhones reignited concerns about international trade friction. This development overshadowed a largely positive corporate earnings period, introducing a cautious tone ahead of the Memorial Day weekend. The key question for investors is whether these renewed trade concerns will prove transient or signal a more sustained headwind for economic growth and corporate profitability.

- U.S. equity benchmarks, including the S&P 500 and Dow Jones Industrial Average, retreated, with the S&P 500's trend deteriorating to negative. This shift, alongside persistently unfavorable outlooks for other broad market segments, suggests heightened investor apprehension.

- Leading U.S. technology firms, notably Apple, faced downward pressure from the prospect of new import taxes. This contributed to a negative shift in the Information Technology sector's trend. In contrast, traditionally defensive areas like Utilities and Consumer Staples demonstrated relative strength, their trends turning positive.

- The assessment of U.S. corporate earnings prospects turned negative, while the outlook for consumer strength moderated to neutral. These changes reflect concerns that tariffs could compress profit margins and dampen economic activity, despite recent underlying resilience.

- Internationally, European equities fell in response to the tariff news. Asian markets, however, showed some buoyancy, partly influenced by policy easing in China. Gold prices increased, likely reflecting a search for safe-haven assets.

MARKET OVERVIEW

Fresh tariff threats targeting European Union imports and Apple iPhones introduced significant market unease on Friday, overshadowing the latter stages of a robust earnings season. This reminder of persistent geopolitical trade risks prompted a risk-off sentiment, leading to an equity market pullback as participants evaluated the potential ramifications. The market's reaction underscores its ongoing sensitivity to trade policy, even against a backdrop of resilient corporate performance. This raises the question of how deeply such policies might disrupt established supply chains and international commerce if fully enacted.

The uncertainty also influenced other asset classes. Bond yields declined, with the 10-year Treasury yield reportedly falling to 4.51%, as concerns grew over potential trade disruptions and their broader economic impact. This movement extended a recent reversal from higher yield levels. The U.S. dollar weakened against major international currencies. In overseas markets, European bourses reacted directly to the tariff threats with declines, while Asian markets benefited from China's new monetary easing measures. Commodity markets presented a mixed picture; crude oil prices advanced, reportedly despite expectations of a potential OPEC+ supply increase, adding another variable to the global economic outlook. While the earnings season has been largely positive, with a significant percentage of S&P 500 companies reportedly beating estimates, the re-emergence of tariff concerns presents a fresh element of caution for investors.

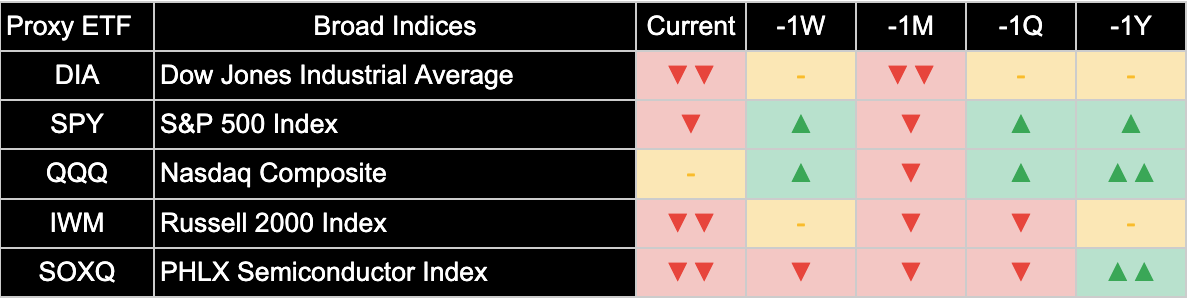

BROAD INDICES

Major U.S. stock indices fell on Friday amid renewed tariff concerns. The S&P 500 Index declined (-0.68%), and its trend shifted to negative from a previously neutral stance. The Dow Jones Industrial Average decreased (-0.59%), maintaining its deeply negative trend. The Nasdaq Composite retreated (-0.93%) but retained its neutral outlook, while the Russell 2000 Index, reflecting smaller company performance, was down (-0.31%) and continued to exhibit a strongly negative trend. The PHLX Semiconductor Index experienced the sharpest daily fall among these benchmarks, declining (-1.46%) and also maintaining a strongly negative trend.

The re-emergence of tariff discussions poses a considerable headwind, potentially eclipsing an otherwise strong earnings season. The negative shift in the S&P 500's trend, combined with persistently weak assessments for several other key indices, signals increasing investor caution. This environment prompts consideration of the durability of recent market strength and whether these trade concerns could translate into a broader economic slowdown, thereby affecting corporate profitability across diverse sectors.

TOP 10 U.S. COMPANIES

Several leading U.S. companies saw their share prices fall on Friday. Apple Inc. experienced a notable daily price drop of (-3.02%), following specific mentions of potential import taxes on iPhones. NVIDIA Corp also declined (-1.16%), and Amazon.com Inc. was down (-1.04%). Microsoft Corp (-1.03%), Meta Platforms Inc (-1.49%), Alphabet Inc (-1.40%), Broadcom Inc (-0.79%), and Tesla Inc (-0.50%) also finished lower. Conversely, JPMorgan Chase & Co recorded a slight gain (+0.02%), while Berkshire Hathaway Inc was nearly unchanged (-0.02%). The trends for Apple Inc. and Amazon.com Inc. remained deeply negative. NVIDIA Corp's trend shifted to negative. Microsoft Corp, Meta Platforms Inc, Alphabet Inc, Tesla Inc, Berkshire Hathaway Inc, and JPMorgan Chase & Co all maintained neutral outlooks. Broadcom Inc. continued to show a positive trend, although its upward momentum appeared to ease.

The direct mention of Apple Inc. in tariff discussions underscores the vulnerability of even the largest U.S. corporations to geopolitical trade tensions. For investors, the negative turn in NVIDIA Corp's trend and the continued weak assessments for Apple Inc. and Amazon.com Inc. suggest that technology and consumer-focused giants are particularly sensitive. This situation necessitates close monitoring of how tariff threats evolve and their potential impact on earnings, especially for companies with significant international operations.

U.S. ECONOMIC INDICATORS

The overarching economic sentiment adopted a cautious tone. The assessment for Investment Duration remained deeply negative, suggesting a challenging environment for assets sensitive to longer-term interest rate expectations. Critically, the outlook for Corporate Earnings shifted to negative, aligning with concerns that new tariffs could pressure profit margins, despite a recently strong earnings reporting period. The view on Inflation held steady at a neutral assessment. Consumer Strength also presented a neutral stance, having weakened from a prior positive assessment, hinting at a potential moderation in consumer-driven economic activity.

The shift to a negative view on corporate earnings is a key development, implying that recent robust profit growth may face headwinds if new tariffs are implemented. This, combined with a persistently unfavorable outlook for investment duration and a softening in consumer strength, suggests increased economic uncertainty. Investors should consider how these factors might influence overall economic growth and whether the current neutral stance on inflation will persist if trade frictions lead to higher input costs.

SECTOR OVERVIEW

Most U.S. sectors retreated on Friday. Information Technology saw a daily price decline of (-1.10%), and its trend shifted to negative. Financials were down (-0.36%), with their trend also turning negative from a previously strong positive. Consumer Discretionary fell (-0.90%), and its trend cooled to neutral. Industrials (-0.33%) also saw their trend move to neutral from strong positive. Materials declined (-0.20%), remaining in a deeply negative trend. Conversely, Consumer Staples gained (+0.37%) and its trend shifted to positive, while Utilities rose (+1.20%), its trend also turning positive. Healthcare (-0.16%) remained in a deeply negative trend. Energy (+0.32%) saw a small gain despite its deeply negative trend. Communication Services fell (-0.46%), and its trend turned negative. Real Estate was nearly flat (+0.02%), its trend remaining deeply negative.

The negative trend shifts in pivotal sectors like Information Technology and Financials, along with cooling trends in Consumer Discretionary and Industrials, suggest a broad market impact from the tariff news. The improved trends for traditionally defensive sectors such as Consumer Staples and Utilities may indicate a flight to perceived safety. This divergence raises questions about market leadership and whether a more defensive posture is warranted if trade tensions escalate.

INTERNATIONAL MARKETS

International market performance was varied. European Union markets traded lower, with the region's proxy declining (-0.16%) following the U.S. tariff statements; despite this, the European Union maintained its strong positive trend. Japan, however, saw gains (+0.91%), and its trend strengthened to strongly positive. China also edged higher (+0.05%), supported by new monetary easing measures, though its trend softened to neutral. India gained (+1.47%), with its trend improving to neutral. Elsewhere, Taiwan's trend turned negative. Hong Kong maintained a positive trend. South Korea’s trend improved to neutral. Singapore continued its strong positive trend. Australia remained neutral. The Middle East & Africa region’s trend cooled to neutral. Emerging Europe's trend turned negative. Canada held its strong positive trend, while Latin America's trend moderated to neutral.

The direct effect of U.S. tariff rhetoric on European markets highlights global economic interconnectedness. Conversely, Japan's strengthening positive trend and China's policy easing showcase differing regional dynamics. This environment calls for a nuanced approach to international allocations, considering specific regional vulnerabilities and policy responses to trade developments.

OTHER ASSETS

Gold was a notable performer, with a daily price increase of (+2.19%); its trend remained positive. Bitcoin, however, experienced a decline (-2.21%), although its trend remained strongly positive. Crude Oil prices rose (+1.27%); its trend remained deeply negative. In fixed income, 1-3 Year Treasury Bonds saw a modest gain (+0.06%), and their trend stayed neutral. 7-10 Year Treasury Bonds also rose (+0.29%), though their trend was negative. 20+ Year Treasury Bonds were up slightly (+0.17%), but their trend remained deeply negative. Industrial Metals gained (+0.70%) with a neutral trend, while Agricultural Commodities fell (-0.95%), also with a neutral trend.

The rally in Gold underscores its traditional role during market stress. The decline in Bitcoin, despite a longer-term positive trend, suggests susceptibility to broad market shocks. Positive price movements in Treasury bonds reflect a flight to quality, aligning with falling yields. Commodity price movements will be watched closely for indications of how trade tensions might impact global supply and demand.

Stay Connected & Share the Insights:

Like this article if you found it helpful.

- Forward this newsletter to colleagues and friends who might find it valuable.

- Subscribe to receive this analysis directly to your inbox.

- Follow us on social media for more updates.

This newsletter is provided for informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security or asset class. The views expressed are those of the author as of the date of publication and are subject to change without notice. Information presented is based on data obtained from sources believed to be reliable, but its accuracy, completeness, and timeliness are not guaranteed. Past performance is not indicative of future results. Investing involves risks, including the possible loss of principal. Readers should consult with their own financial advisors before making any investment decisions. The author and associated entities may hold positions in the assets or asset classes discussed herein.

Join the official LINE account of "Joe’s Wall Street Pulse" now to receive the latest column updates (click here to join)