科技類股領漲大盤 財政部長描繪貿易關係「美麗再平衡」願景

Joe Lu, CFA 2025年4月23日 美東時間

市場概況

由於川普政府繼續暗示美中貿易談判可能有所進展,同時也緩和了近期圍繞美國聯準會獨立性的緊張關係,週三市場延續反彈走勢。政府主要官員較爲和緩的語調激發了投資者對貿易敵對狀態可能緩和的樂觀情緒,這些緊張關係自四月初以來一直對市場造成嚴重壓力。

標普500指數上漲+1.55%收於5,375.86點,納斯達克綜合指數因擁有重大中國業務的科技公司強勁反彈,大漲+2.27%收於16,708.05點,表現優於其他主要指數。道瓊工業平均指數上漲+1.03%收於39,606.57點,羅素2000指數上揚+1.48%,顯示小型股也參與了這場廣泛反彈。然而,因投資者評估反彈的可持續性,市場收盤遠低於盤中高點,主要指數在下午交易中回吐了早盤漲幅的約一半。

今日市場積極走勢主要受到川普總統鼓舞人心的言論而推動。川普總統表示,目前對中國進口商品145%的關稅稅率「在未來不會那麼高」並將「大幅下降」,同時財政部長史考特·貝森特概述了他所稱的世界兩大經濟體之間潛在「美麗再平衡」的願景。貝森特在國際金融協會發表演說時強調,「這是一個達成重大協議的機會」,並表示兩國可以共同重新平衡各自經濟。此外,投資者對美國聯準會獨立性的擔憂在川普總統表示「無意」解雇美國聯準會主席鮑爾後大大緩解,這代表了他近日嚴厲批評的重大轉變。《華爾街日報》報導稱政府正考慮將中國關稅降至50%至65%之間,進一步證明方法美國政府可能改變方針,不過一位白宮官員隨後澄清,任何降稅都需要雙邊同時進行。

摘要:

- 市場延續週二漲勢,標普500指數上漲+1.55%,納斯達克大漲+2.27%,因川普總統表示中國關稅將「大幅下降」

- 科技類股領漲,上揚+2.98%,緊隨其後的是「輝煌七雄」股票,整體攀升+3.35%,具有重大中國業務的公司受益

- 財政部長貝森特在IIF論壇上概述了潛在的「美麗再平衡」美中貿易關係願景

- 川普總統緩解了對美國聯準會獨立性的擔憂,表示「無意」在鮑威爾2026年任期結束前撤換他

- 費城半導體指數大漲+3.81%,因最易受中國貿易緊張局勢影響的科技硬體公司反彈最強勁

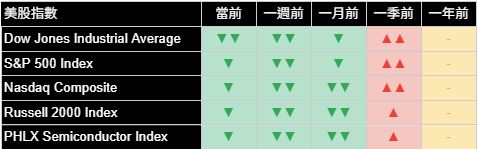

廣泛市場指數

主要指數連續第二個交易日全面大幅上漲,成長導向類股表現出明顯的領導模式。納斯達克綜合指數上漲+2.27%,超越其他主要基準指數,反映受貿易緊張局勢影響較大的科技股及成長股表現尤其強勁。標普500指數上漲+1.55%,展現了跨多個類股的廣泛參與,但表現有明顯差異。

費城半導體指數飆升+3.81%,為主要指數中最強勁的表現,原因是與中國供應鏈及市場有重大關係的公司大幅反彈。羅素2000小型股指數上漲+1.48%,繼續落後於大型科技股表現,但在週二反彈後保持積極動能。道瓊工業平均指數相對溫和的+1.03%漲幅,反映其對科技股的曝險較低和對防禦型類股的較高集中度,這些類股在強勁風險偏好環境下表現通常不佳。

儘管兩天的穩健反彈,大多數主要指數的趨勢模式仍令人擔憂,在目前、一週和一個月時間框架內均呈現負面讀數。然而,標普500指數和納斯達克正顯示出每日和每週動能改善的早期跡象,積極的變化讀數暗示市場動態可能趨於穩定。這種持續負面趨勢與改善短期動能之間的新興分歧,代表了潛在的轉折點。如果得到貿易談判具體進展或政府政策明確性的支持,這可能標誌著更可持續復甦的開始。

美國十大公司

美國大型股在週三展現出令人印象深刻的強勢,輝煌七雄科技龍頭股整體上漲+3.35%,明顯優於大盤。這一強勁表現暗示機構投資者在近期防禦性配置後,開始向成長領導股重新部署資金,特別是那些最受美中貿易緊張局勢影響的公司。

特斯拉領漲,上揚+5.37%,同時受益於改善的貿易情緒和執行長馬斯克(Elon Musk)的言論,他表示從下個月起,在政府效率部(DOGE)的工作時間將「顯著」減少。亞馬遜(+4.28%)、博通(+4.32%)和Meta平台(+4.00%)也表現超出預期的漲幅,均明顯優於大盤。蘋果(+2.43%)和微軟(+2.06%)為較溫和但仍然可觀的漲幅。科技生態系統內不同商業模式的表現相對平衡,暗示市場對成長前景廣泛的重新評估,而非特定公司發展推動今日的市場行動。

儘管近期上漲,大多數大型公司在目前、一週和一個月時間框架內仍顯示負面趨勢,反映四月拋售期間遭受的嚴重技術性損害。然而,包括特斯拉、博通和亞馬遜在內的幾家龍頭公司正顯示出積極的每日和每週變化讀數,暗示動能正在改善。若持續下去,最終可能轉化為更具建設性的趨勢模式。值得注意的是,波克夏海瑟威在市場動盪中繼續展現相對穩定的表現,其積極的季度趨勢突顯了其多元化商業模式和充足現金儲備在政策不確定時期的價值。

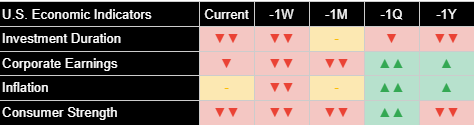

經濟指標

儘管市場近期穩定,經濟指標仍呈現出複雜局面,關鍵指標的改善幅度有限。

公司獲利指標在每日和每週讀數中顯示出適度改善,此前有所惡化,這可能反映穩健的第一季度業績,表明儘管面臨貿易擔憂,企業基本面仍相對穩健。這種適度積極的企業表現與更負面的經濟情緒之間的差異突顯了美國公司在政策逆風下的韌性,不過持續的貿易緊張可能最終會對獲利造成更直接的壓力,正如幾家跨國公司近期指引所示。

消費者信心在多個時間框架內繼續呈現持續疲弱,顯示市場持續擔憂貿易動態和政策不確定性對家庭支出模式和信心的影響。考慮到消費對美國經濟增長的重要性,消費者指標的疲弱對經濟前景構成重大風險。如果缺乏更實質性的政策明確性,可能會限制市場反彈的持久性。前瞻性指標暗示,除非貿易談判顯示有意義的進展,否則這種消費者謹慎的態度可能持續到夏季,可能影響第二季度零售銷售和相關經濟數據。

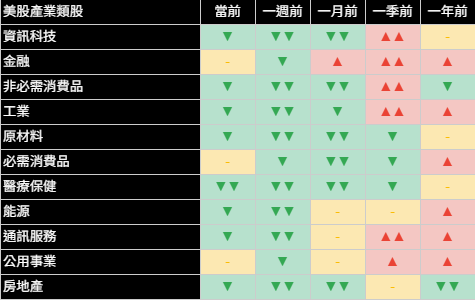

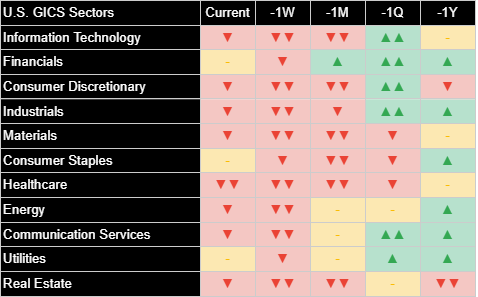

類股概況

週三交易中,標普500指數大多數類股表現積極,漲幅差異極大,明確顯示出成長導向類別的領導地位。資訊科技類股以+2.98%的漲幅領漲,反映出對科技需求的樂觀情緒重新湧現,以及貿易相關供應鏈中斷的可能降低。非必需消費品(+2.23%)和通信服務(+1.60%)也優於大盤表現,周期性成長類股從近期低點強勁反彈。

表現最弱的是必需消費品(-0.57%)和能源(-0.18%),是當天唯一下跌的類股。這種表現模式代表了從近期市場疲弱期間的防禦性領導轉變,隨著風險偏好改善,投資者從安全資產轉向成長。金融(+1.19%)、工業(+1.25%)和原物料(+0.12%)取得較為溫和的漲幅,反映出對經濟敏感類股的謹慎配置,這些類股將受到長期貿易爭端的最直接影響。

儘管今日上漲,類股趨勢在目前、一週和一個月時間框架內仍主要呈現負面,不過科技、非必需消費品和通信服務等幾個類股,皆顯示出積極的每日變化讀數。這種短期動能的新興改善可能暗示,如果得到持續的政策明確性和貿易進展支持,趨勢穩定化可能開始。周期性和防禦性表現之間的顯著差異支持風險偏好改善的敘事,但工業和原物料相對溫和的漲幅表明投資者仍然選擇性投資,而非廣泛擁抱經濟敏感類股。

國際市場

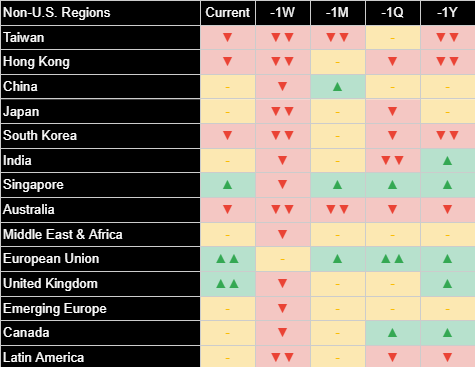

週三全球市場展現廣泛強勁,特別是那些最受美中貿易動態影響的地區表現尤為出色。MSCI中國指數上漲+1.49%,延續最近的漲勢,因投資者繼續評估在川普總統和財政部長貝森特言論後貿易緩和的可能性。台灣+0.81%的小幅上漲,反映出對半導體供應鏈環境可能改善的謹慎樂觀。

歐洲市場表現出溫和強勁,歐盟指數上漲+0.34%,英國上漲+0.27%。與美國和亞洲市場相比,這種相對低迷的表現表明,儘管美中關係可能有所改善,歐洲投資者對更廣泛的全球成長前景仍然有些謹慎。日本上漲+0.30%,韓國保持平穩,儘管它們對全球貿易流動有重大曝險,兩者均顯示出比美國市場更為克制的反應。

新興市場表現參差不齊,拉丁美洲上漲+1.12%,印度下跌-0.60%。新興亞洲上漲+0.91%,因該地區普遍受益於對中國成長前景情緒的改善,不過各市場間差異顯著。新興市場的各種表現突顯了潛在貿易政策轉變的複雜影響,因投資者重新評估全球供應鏈動態和區域成長差異,商品出口國通常優於製造業經濟體。

其他資產

跨資產市場顯示配置發生顯著轉變,傳統避險資產隨著風險偏好改善而回撤。黃金下跌-2.40%,因傳統避險資產需求減弱,從本週早些時候創下的紀錄高點繼續回調。比特幣上漲+2.15%,在更廣泛的風險情緒改善中保持近期強勢,繼續展示其作為替代價值儲存和投機性成長資產的日益多元化角色。

美國國債價格呈現混合模式,長期債券上漲,短期債券略微下跌。20年期以上國債上漲+0.97%,殖利率曲線略微平坦化,可能反映出儘管近期政策趨於穩定,但對長期增長放緩的預期。7-10年期債券上漲+0.11%,1-3年期國債下跌-0.07%。殖利率曲線的這種混合表現表明,隨著貿易政策演變,投資者正重新評估通膨風險與成長擔憂之間的平衡,較長期限債券受益於關稅前景緩和帶來的略微降低通膨預期。

美元指數溫和走強,因財政部長貝森特概述了他對全球金融體系改革的願景,而大多數商品類別表現不一。原油下跌-1.90%,因對全球經濟成長的擔憂仍超過地緣政治供應風險。而工業金屬上漲+1.16%,受潛在貿易緩和後製造業前景改善推動。農產品基本持平,為-0.04%,反映出在各種關稅情境下對農業貿易流動可能變化的持續不確定性。

總結來說,週三市場行動反映出投資者情緒在美中貿易緊張和政府對美國聯準會獨立性批評可能趨向緩和的跡象後繼續改善。財政部長貝森特概述的世界兩大經濟體「美麗再平衡」為持續談判提供了建設性框架,而川普總統表示「無意」解雇美國聯準會主席鮑爾,則幫助緩解了對貨幣政策獨立性的擔憂。然而,市場從盤中高點部分回撤表明投資者對近期改善的可持續性仍持謹慎態度,多個經濟指標仍顯示出受近期政策波動造成的不確定性影響的跡象。短期經濟動能的改善與中期持續負面趨勢之間的差異,突顯了當前復甦的條件性質,這可能需要持續的政策明確性和貿易談判的具體進展才能維持市場上揚軌跡。

關於《Joe’s 華爾街脈動》

鉅亨網特別邀請到擁有逾 22 年美國投資圈資歷、CFA 認證的機構操盤人 Joseph Lu 擔任專欄主筆。

Joe 為台裔美國人,曾管理超過百億美元規模的基金資產,並為總資產高達數千億美元的多家頂級金融機構提供資產配置優化建議。

Joe 目前帶領著由美國頂尖大學教授與博士組成的精英團隊,透過獨家開發的 "趨勢脈動 TrendFolios® 指標",為台灣投資人深度解析全球市場脈動,提供美股市場第一手專業觀點,協助投資人掌握先機。

Markets Extend Gains as Trump Signals Softer Stance on China Tariffs and Fed Chair's Future

Tech Leads Broad-Based Rally While Treasury Secretary Outlines Vision for "Beautiful Rebalancing" in Trade Relations

Joe Lu, CFA April 23, 2025

MARKET OVERVIEW

Markets extended their recovery on Wednesday as the Trump administration continued to signal a potential path forward in US-China trade negotiations, while also easing recent tensions concerning Federal Reserve independence. The more conciliatory tone from key administration officials sparked renewed investor optimism about the potential for de-escalation in trade hostilities that have weighed heavily on markets since early April.

The S&P 500 advanced +1.55% to close at 5,375.86, while the Nasdaq Composite surged +2.27% to end at 16,708.05, outperforming other major indices as technology companies with significant Chinese exposure rallied strongly. The Dow Jones Industrial Average gained +1.03% to finish at 39,606.57, and the Russell 2000 rose +1.48% as smaller companies participated in the broad-based rally. However, markets finished well off their intraday highs, with the major indices giving back roughly half their earlier gains during afternoon trading as investors assessed the sustainability of the rebound.

Today's positive market action was primarily driven by encouraging comments from President Trump, who stated the current 145% tariff rate on Chinese imports "won't be anywhere near that high" and will "come down substantially," while Treasury Secretary Scott Bessent outlined his vision for what he called a potential "beautiful rebalancing" between the world's two largest economies. Bessent, speaking at the Institute of International Finance forum, emphasized that "there is an opportunity for a big deal here" and suggested both countries could rebalance their economies together. Additionally, investor concerns about Federal Reserve independence eased considerably after President Trump stated he has "no intention" of firing Fed Chair Jerome Powell, representing a significant reversal from his harsh criticism in recent days. The Wall Street Journal's report that the administration is considering reducing Chinese tariffs to between 50% and 65% provided further evidence of a potential shift in approach, though a White House official later clarified that any reduction would need to be bilateral.

Executive Summary:

- Markets built on Tuesday's momentum with S&P 500 gaining +1.55% and Nasdaq surging +2.27% as President Trump indicated China tariffs will "come down substantially"

- Technology segment led advances with +2.98% gain, followed by Magnificent Seven stocks which jumped +3.35% as companies with significant China exposure benefited

- Treasury Secretary Bessent outlined vision for potential "big beautiful rebalancing" in US-China trade relations at IIF forum

- President Trump eased concerns about Fed independence, stating he has "no intention" of removing Powell before his term ends in 2026

- Philadelphia Semiconductor Index surged +3.81% as technology hardware firms most exposed to China trade tensions posted strongest recoveries

BROAD MARKET INDICES

Major indices recorded solid gains across the board for a second consecutive session, with a clear leadership pattern emerging among growth-oriented segments. The Nasdaq Composite's +2.27% advance outpaced other major benchmarks, reflecting particularly strong performance in technology and growth stocks that had been disproportionately affected by trade tensions. The S&P 500's +1.55% gain demonstrated broad participation across multiple segments, though with meaningful dispersion in performance.

The Philadelphia Semiconductor Index surged +3.81%, recording the strongest performance among major indices as companies with significant exposure to Chinese supply chains and markets rebounded sharply. The Russell 2000 small-cap index gained +1.48%, continuing to lag the performance of large-cap technology but maintaining positive momentum following Tuesday's recovery. The Dow Jones Industrial Average's relatively modest +1.03% advance reflected its lower exposure to technology and greater concentration in more defensive segments that typically underperform during strong risk-on sessions.

Despite the solid two-day recovery, trend patterns for most major indices remain concerning, with negative readings across current, one-week, and one-month timeframes. However, the S&P 500 and Nasdaq are showing early signs of improving daily and weekly momentum, with positive delta readings suggesting potential stabilization in market dynamics. This emerging divergence between persistent negative trends and improving short-term momentum represents a potential inflection point that could signal the beginning of a more sustainable recovery if supported by concrete progress in trade negotiations or policy clarity from the administration.

TOP 10 U.S. COMPANIES

The largest U.S. companies demonstrated impressive strength on Wednesday, with the Magnificent Seven technology leaders advancing +3.35% as a group, significantly outperforming the broader market. This robust performance suggests institutional investors are beginning to redeploy capital toward growth leaders after recent defensive positioning, particularly in names most affected by US-China trade tensions.

Tesla led the advance with an impressive +5.37% gain, benefiting from both improved trade sentiment and CEO Elon Musk's comments that his time spent running the administration's Department of Government Efficiency would "significantly" decrease next month. Amazon (+4.28%), Broadcom (+4.32%), and Meta Platforms (+4.00%) also posted outsized gains, all meaningfully outperforming the broader market. Apple (+2.43%) and Microsoft (+2.06%) recorded more modest but still substantial advances. The relatively balanced performance across different business models within the technology ecosystem suggests a broad-based reassessment of growth prospects rather than company-specific developments driving today's market action.

Most of the largest companies continue to show negative trends across current, one-week, and one-month timeframes despite recent gains, reflecting the significant technical damage inflicted during the April selloff. However, several leaders including Tesla, Broadcom, and Amazon are showing positive daily and weekly delta readings, suggesting improving momentum that could eventually translate into more constructive trend patterns if sustained. Notably, Berkshire Hathaway continues to demonstrate relatively stable performance amid market turbulence, with positive quarterly trends highlighting the value of its diversified business model and substantial cash reserves during periods of policy uncertainty.

ECONOMIC INDICATORS

Economic measures continue to present a mixed picture despite recent market stabilization, with only limited improvement visible in key indicators.

Corporate earnings measures have shown modest improvement in daily and weekly readings after recent deterioration, potentially reflecting solid first-quarter results that suggest fundamentals remain relatively healthy despite trade concerns. This divergence between moderately positive corporate performance and more negative economic sentiment highlights the resilience of US companies in the face of policy headwinds, though sustained trade tensions could eventually pressure earnings more directly as suggested by recent guidance from several multinational corporations.

Consumer strength continues to show persistent weakness across multiple timeframes, indicating ongoing concern about how trade dynamics and policy uncertainty might affect household spending patterns and confidence. This weakness in consumer measures presents a meaningful risk to the economic outlook given the importance of consumption to US economic growth, potentially limiting the durability of any market recovery absent more substantial policy clarity. Forward-looking indicators suggest this consumer caution could persist into summer unless trade negotiations show meaningful progress, potentially affecting second-quarter retail sales and related economic data.

SECTOR OVERVIEW

Wednesday's trading saw positive performance across most S&P 500 segments, with substantial divergence in magnitude of gains revealing clear leadership from growth-oriented categories. The Information Technology segment led advances with a gain of +2.98%, reflecting renewed optimism about technology demand and potential reduction in trade-related supply chain disruptions. Consumer Discretionary (+2.23%) and Communication Services (+1.60%) also outperformed the broader market as cyclical growth segments bounced strongly from recent lows.

The weakest performers were Consumer Staples (-0.57%) and Energy (-0.18%), the only segments to record losses on the day. This performance pattern represents a clear reversal from defensive leadership during recent market weakness, with investors rotating away from safety and back toward growth as risk appetite improves. Financials (+1.19%), Industrials (+1.25%), and Materials (+0.12%) recorded more modest gains, reflecting still-cautious positioning in economically sensitive segments that would be most directly impacted by a prolonged trade dispute.

Sector trends remain predominantly negative across current, one-week, and one-month timeframes despite today's gains, though several segments including Technology, Consumer Discretionary, and Communication Services are showing positive daily delta readings. This emerging improvement in short-term momentum could potentially signal the beginning of trend stabilization if supported by continued policy clarity and trade progress. The significant divergence between cyclical and defensive performance today supports the narrative of improving risk appetite, though the relatively modest gains in industrials and materials suggest investors remain selective rather than broadly embracing economically sensitive segments.

INTERNATIONAL MARKETS

Global markets demonstrated broad strength on Wednesday, with particularly strong performance in regions most exposed to US-China trade dynamics. MSCI China advanced +1.49%, extending recent gains as investors continued to assess the potential for trade de-escalation following comments from both President Trump and Treasury Secretary Bessent. Taiwan posted a modest gain of +0.81%, reflecting cautious optimism about potential improvements in the semiconductor supply chain environment.

European markets showed modest strength, with the European Union index gaining +0.34% and the United Kingdom advancing +0.27%. This relatively subdued performance compared to US and Asian markets suggests European investors remain somewhat cautious about the broader global growth outlook despite potential improvement in US-China relations. Japan gained +0.30% and South Korea remained flat, both showing more restrained reactions than US markets despite their significant exposure to global trade flows.

Emerging markets demonstrated mixed performance, with Latin America gaining +1.12% while India declined -0.60%. Emerging Asia advanced +0.91% as the region broadly benefited from improved sentiment toward Chinese growth prospects, though with considerable dispersion among individual markets. The varied performance across emerging markets highlights the complex impact of potential trade policy shifts, with commodity exporters generally outperforming manufacturing economies as investors reassess global supply chain dynamics and regional growth differentials.

OTHER ASSETS

The cross-asset landscape revealed a significant shift in market positioning as traditional safe havens retreated amid improved risk appetite. Gold fell -2.40%, continuing its correction from record highs set earlier in the week as demand for traditional safehaven assets moderated. Bitcoin gained +2.15%, maintaining its recent strength amid the broader improvement in risk sentiment and continuing to demonstrate its increasingly diverse role as both alternative store of value and speculative growth asset.

Treasury prices showed a mixed pattern, with long-term bonds advancing while shorter maturities declined slightly. The 20+ year Treasury segment gained +0.97% as the yield curve flattened modestly, potentially reflecting expectations for slower long-term growth despite near-term policy stabilization. The 7-10 year segment rose +0.11%, while the 1-3 year Treasury segment declined -0.07%. This mixed performance across the curve suggests investors are reassessing the balance between inflation risks and growth concerns as trade policy evolves, with longer maturities benefiting from slightly reduced inflation expectations as tariff prospects moderate.

The U.S. Dollar Index strengthened moderately as Treasury Secretary Bessent outlined his vision for global financial system reforms, while most commodity categories showed mixed performance. Crude oil declined -1.90% as global growth concerns continued to outweigh geopolitical supply risks, while industrial metals gained +1.16% on improved manufacturing outlook following potential trade de-escalation. Agricultural commodities remained essentially flat at -0.04%, reflecting ongoing uncertainty about potential changes to agricultural trade flows under various tariff scenarios.

In summary, Wednesday's market action reflected continued improvement in investor sentiment following signs of potential de-escalation in both US-China trade tensions and the administration's criticism of Federal Reserve independence. Treasury Secretary Bessent's outline of a potential "beautiful rebalancing" between the world's two largest economies provided a constructive framework for ongoing negotiations, while President Trump's statement that he has "no intention" of firing Fed Chair Powell helped ease concerns about monetary policy independence. However, the market's partial retracement from intraday highs suggests investors remain cautious about the sustainability of recent improvements, with multiple economic indicators still showing signs of strain from the uncertainty created by recent policy volatility. The divergence between improving short-term momentum and persistently negative medium-term trends highlights the conditional nature of the current recovery, which likely requires continued policy clarity and concrete progress in trade negotiations to sustain its upward trajectory.