•

【Joe’s華爾街脈動】標普500指數結束連九漲,關稅協議不確定性打壓市場

服務業數據強勁,市場回檔;聯準會會議在即

Joe Lu, CFA 2025年5月5日 美東時間

市場概況

美國股市週一開盤走低,市場回檔,結束了標普500指數令人矚目的連續九天漲勢。此次下跌反映了投資者的謹慎態度,儘管政府官員持續評論稱協議已近,但圍繞潛在貿易協議的時機和具體細節仍存在持續的不確定性。雖然財政部長Bessent重申美國「非常接近達成某些協議」,可能就在本週,但川普總統隨後發表的言論表示並未安排與中國國家主席習近平會談,且宣布可能對外國製作的影劇加徵100%關稅,這都加劇了貿易政策上複雜且時而矛盾的訊號。這種缺乏實質進展的局面似乎正使推動上週反彈的樂觀情緒逐漸降溫。

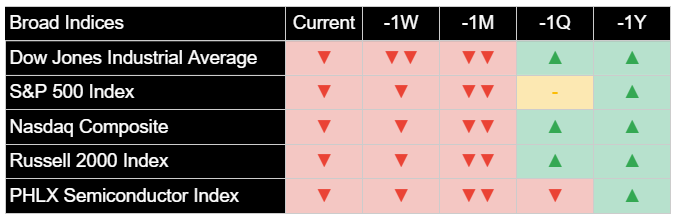

主要美股指數從近期高點回落。標普500指數下跌-0.57%,結束了自2004年以來最長的連漲紀錄。道瓊工業平均指數下跌-0.19%,以科技股為主的那斯達克綜合指數則下跌-0.59%。以羅素2000指數為代表的小型股同樣下跌,跌幅為-0.77%。指數從盤中低點收窄跌幅,推測可能部分受到印度提議某些互惠零關稅措施報導的幫助,但整體氛圍仍偏保守。

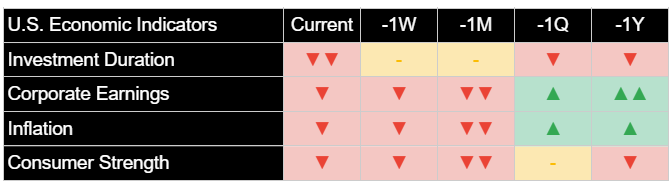

今日公布的經濟數據呈現出好壞參半的景象。美國供應管理協會(ISM)四月份服務業PMI指數為51.6,優於預期的50.4,顯示關鍵的服務業仍持續擴張。然而,報告細節突顯了物價上漲壓力(支付價格指數顯著跳升),並反映出受訪者日益擔憂關稅對成本和業務營運的衝擊。此數據凸顯了美國聯準會在明天開始為期兩天的政策會議時所面臨的艱鉅挑戰,需要在某些領域具韌性的經濟活動、受貿易政策加劇的潛在通膨壓力,以及先前指出的消費者壓力跡象之間取得平衡。

重點摘要

- 主要美股指數週一下跌,因關稅協議的不確定性打壓市場情緒,結束了標普500指數 (-0.57%) 連續九天的漲勢:標普500指數 (-0.57%),道瓊工業平均指數 (-0.19%),那斯達克綜合指數 (-0.59%)。

- 儘管近期上漲,根據分析,潛在的近期市場特性普遍仍屬不利,表明此波反彈尚未得到更深層趨勢的充分確認。

- 美國供應管理協會(ISM)四月份服務業採購經理人指數(PMI)優於預期,顯示該產業具韌性,但也突顯企業面臨物價上升的壓力和關稅方面的擔憂。

- 多數類股回檔,由能源 (-1.81%) 和資訊科技 (-0.68%) 領跌。公債價格漲跌互見;黃金價格強勁上漲。

- 市場注意力轉向明天開始的美國聯準會為期兩天的政策會議,投資者關注其關於通膨、成長及貿易政策影響的評論。

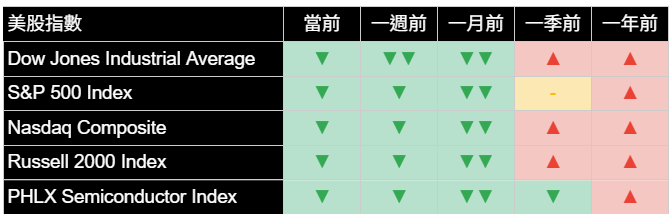

主要市場指數

費城半導體指數當日亦下跌,跌幅為-0.92%。儘管參與了近期的反彈,但潛在分析持續顯示,該族群在多個時間區間內仍處於明顯不利的狀況。

從分析角度來看,今日的下跌進一步支持了我們對近期市場整體不利特徵的既有判斷。儘管先前動能強勁,但未能延續上週的漲勢,表明先前觀察到的潛在負面訊號尚未被消除。市場狀況尚未出現可持續改善的明確確認訊號,支持採取謹慎立場。

美國前十大公司

美國大型企業週一表現普遍疲弱,反映出更廣泛的市場回檔以及與貿易政策公告相關的特定擔憂。

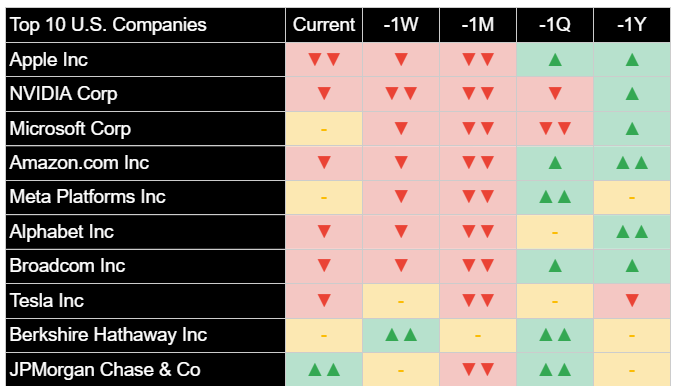

觀察個股當日表現:波克夏海瑟威B股 (Berkshire Hathaway Inc Class B) 大跌-5.12%,股價從歷史高點大幅回落,主因為週末傳出華倫·巴菲特計劃在年底卸任執行長的消息。科技和通訊類股也普遍走弱。據報導,Netflix(雖非前十大,但受電影關稅消息影響)下跌,可能拖累了串流媒體類股的市場情緒。在前十大公司中,亞馬遜 (Amazon.com Inc) 下跌-1.91%,蘋果 (Apple Inc) 回檔-3.15%,特斯拉 (Tesla Inc) 下跌-2.42%,博通 (Broadcom Inc) 下跌-1.43%,輝達 (NVIDIA Corp) 下滑-0.59%。Alphabet Inc A股 (Alphabet Inc Class A) 微幅上漲+0.11%,微軟 (Microsoft Corp) 亦上漲+0.20%。Meta Platforms Inc 也上漲+0.38%。摩根大通 (JPMorgan Chase & Co) 小幅上漲+0.02%。

根據我們的分析指標去解讀潛在的分析訊號,這些領先企業中大多數的近期市場特性仍偏向疲弱或中性。今日普遍負面的價格走勢與這種潛在的謹慎基調相符。波克夏海瑟威的急跌反映了特定的公司消息,而其他大型股的疲弱則突顯了對整體市場情緒與貿易政策風險的敏感性。

經濟指標

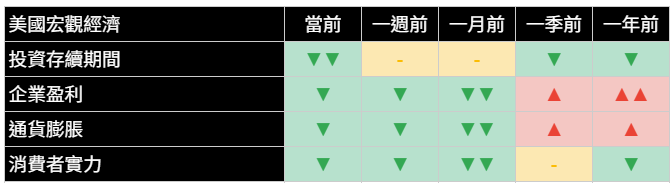

今日的主要經濟數據點——四月份ISM服務業PMI——為投資者和決策者傳遞了複雜的訊息。指數報51.6,顯示服務業擴張優於預期,表明儘管存在經濟逆風,該產業仍具韌性。然而,報告中的部分細項引發了擔憂:支付價格指數飆升,顯示該產業內部通膨壓力加劇,且多位受訪者的評論中頻繁提及關稅帶來的不確定性和負面衝擊。

這項官方數據為我們的整套經濟指標提供了背景參考。強勁的ISM活動數據與我們分析中近期觀察到的投資存續期間中性訊號某種程度上一致,表明市場並未預示立即崩盤。然而,ISM調查中價格組成部分的上升,可能對我們近期在通膨指標訊號中觀察到的緩和趨勢構成挑戰,後續需密切關注。此外,來自我們消費者信心指標持續疲弱的訊號仍是一個擔憂點,這也與一些服務業受訪者的保守看法以及上週疲弱的信心數據相符。從市場分析推估出的企業獲利前景持續顯得低迷。總體而言,經濟景象依然複雜,服務業活動雖具韌性,但面臨成本壓力上升和關稅衝擊,使得聯準會會議前的經濟前景更加難以判斷。

類股概況

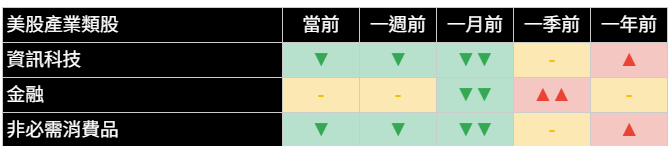

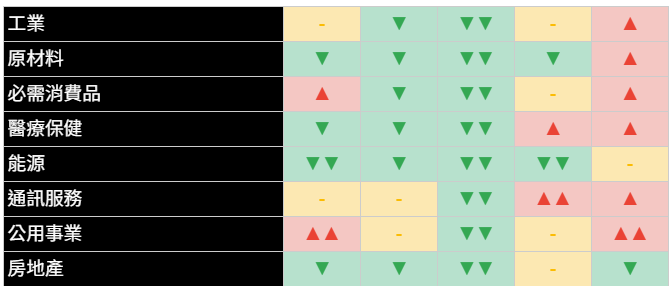

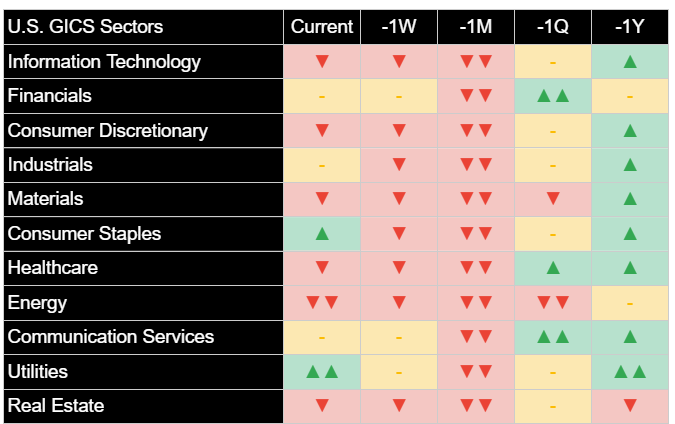

隨著市場連漲告終,風險規避的基調反映在週一標準普爾500指數各類股普遍轉弱的表現上。十一個類股中有十個收低,週期性和科技相關族群普遍領跌。

能源類股 (-1.81%) 表現最差,可能受到全球需求的持續擔憂持續升溫以及先前交易日原油價格走弱的壓力所致。資訊科技類股 (-0.68%) 也顯著下跌。非必需消費品類股 (-1.06%) 回檔,與對消費者支出的持續擔憂一致。原物料類股 (-0.74%) 和金融類股 (-0.64%) 亦下跌。防禦型類股提供了相對而非絕對的避風港:公用事業類股 (-0.25%)、房地產類股 (-0.36%) 和醫療保健類股 (-0.28%) 跌幅較小。必需消費品類股 (-0.09%) 收盤近乎持平,展現出最強的韌性。唯一實現上漲的類股是工業類股 (+0.05%)。

從分析角度來看,今日多數類股的普遍下跌,進一步支持了我們分析所顯示的多數市場領域近期狀況不利或中性的看法。防禦型類股的相對強勢與潛在的謹慎基調一致。若週期性和成長型類股持續疲軟,將進一步印證我們指標所顯示的負面近期前景。

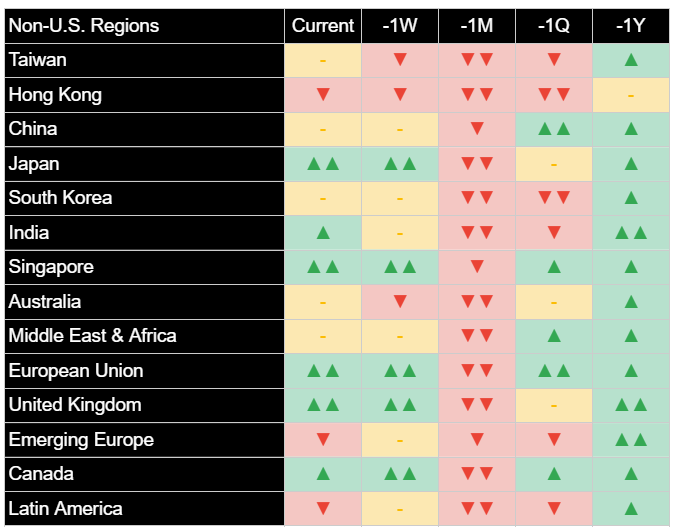

國際市場

跟隨美國市場的負面帶動,國際市場週一亦經歷回檔,並反映了對全球貿易不確定性的共同擔憂。美元當日微幅走強,上漲+0.11%。

已開發市場下跌:歐洲股市下跌-0.49%,日本股市下跌-0.64%。儘管近期的分析顯示特性有所增強,但這些市場對來自美國的全球風險情緒和貿易發展依然敏感。

新興市場也普遍走低:新興亞洲市場下跌-1.11%,印度下跌-0.76%,拉丁美洲下跌-1.00%。中國股市回檔-0.04%,相對表現略好,但最終仍收低。廣泛的跌勢突顯了圍繞貿易政策衝擊的擔憂具有全球性。

其他資產

週一其他資產類別的活動普遍反映了謹慎、避險的情緒。債券價格漲跌互見,多數大宗商品下跌,黃金則逆勢上漲,美元微幅走強。

在固定收益方面,美國公債價格漲跌互見。短期公債價格微幅下跌 (-0.01%),而中期公債價格 下跌-0.18%。長期公債價格則逆勢上漲,錄得+0.04%的漲幅。整體美國綜合債券價格下跌-0.15%。這表明儘管股市回檔,但尋求避險的需求有限。

大宗商品表現大多為負,僅有一項顯著例外。WTI原油下跌-2.56%。基本金屬上漲+0.22%。農產品下跌-0.56%。值得注意的是,黃金價格飆升+2.99%,在股市回檔和貿易不確定性中扮演了避險資產的角色。美元指數微幅走強,上漲+0.11%。在數位資產方面,比特幣價格下跌-2.83%,與其他風險資產同步走低。

立即加入《Joe’s 華爾街脈動》LINE@官方帳號,獲得最新專欄資訊(點此加入)

關於《Joe’s 華爾街脈動》

鉅亨網特別邀請到擁有逾 22 年美國投資圈資歷、CFA 認證的機構操盤人 Joseph Lu 擔任專欄主筆。 Joe 為台裔美國人,曾管理超過百億美元規模的基金資產,並為總資產高達數千億美元的多家頂級金融機構提供資產配置優化建議。 Joe 目前帶領著由美國頂尖大學教授與博士組成的精英團隊,透過獨家開發的 "趨勢脈動 TrendFolios® 指標",為台灣投資人深度解析全球市場脈動,提供美股市場第一手專業觀點,協助投資人掌握先機。

S&P 500 Snaps Nine-Day Winning Run as Uncertainty on Tariff Deals Weighs on Markets

Markets Pull Back Amid Strong Services Data, Fed Meeting Looms

Joe Lu, CFA May 5, 2025

MARKET OVERVIEW

U.S. equity markets started the week on a negative note, pulling back on Monday and halting the S&P 500's impressive nine-day winning streak. The decline reflected investor caution amidst ongoing uncertainty regarding the timing and specifics of potential trade deals, despite continued commentary from administration officials suggesting agreements are close. While Treasury Secretary Bessent reiterated that the U.S. is "very close to some deals," possibly this week, President Trump's subsequent remarks indicating no planned talks with China's President Xi and announcing potential 100% tariffs on foreign-produced films added to the complex and sometimes contradictory signaling on trade policy. This lack of concrete progress appears to be tempering the optimism that fueled last week's rally.

The major U.S. stock indices retreated from recent highs. The S&P 500 Index shed -0.57%, ending its longest winning run since 2004. The Dow Jones Industrial Average dropped -0.19%, and the technology-heavy Nasdaq Composite Index fell -0.59%. Small-capitalization stocks, represented by the Russell 2000 Index, also declined, losing -0.77%. Indices pared losses from session lows, potentially aided by reports that India has proposed some reciprocal zero-tariff measures, but the overall tone remained cautious.

Economic data released today presented a mixed picture. The Institute for Supply Management (ISM) Services PMI for April came in stronger than expected at 51.6 (versus 50.4 forecast), indicating continued expansion in the crucial services sector. However, the report's details highlighted rising price pressures (prices paid index jumped significantly) and reflected growing concerns among respondents about the impact of tariffs on costs and business operations. This data underscores the challenging environment the Federal Reserve faces as it begins its two-day policy meeting tomorrow, balancing resilient activity in some areas with potential inflation pressures exacerbated by trade policy and signs of consumer strain noted previously.

EXECUTIVE SUMMARY

- Major U.S. indices declined Monday, ending the S&P 500's nine-day winning streak as tariff deal uncertainty weighed on sentiment: S&P 500 Index (-0.57%), Dow Jones Industrial Average (-0.19%), Nasdaq Composite Index (-0.59%).

- Despite recent gains, underlying near-term market character remained broadly unfavorable according to analysis, suggesting the rally lacked full confirmation from deeper trends.

- ISM Services PMI beat expectations in April, showing sector resilience, but also highlighted rising price pressures and tariff concerns among businesses.

- Most sectors retreated, led lower by Energy (-1.81%) and Information Technology (-0.68%). Treasury prices were mixed; Gold gained strongly.

- Attention shifts to the Federal Reserve's two-day policy meeting starting tomorrow, with investors focused on commentary regarding inflation, growth, and trade policy impacts.

BROAD MARKET INDICES

Broad market indices declined across the board on Monday, snapping the recent winning streak for the S&P 500. The S&P 500 Index fell -0.57%, the Dow Jones Industrial Average lost -0.19%, the Nasdaq Composite Index dropped -0.59%, and the Russell 2000 Index retreated -0.77%. The pullback suggests investors are pausing to reassess the outlook following the strong run-up, particularly given the lingering uncertainty surrounding trade negotiations and ahead of the Federal Reserve's policy decision.

The PHLX Semiconductor Index also declined, falling -0.92% on the day. Despite participating in the recent rally, underlying analysis for this group continues to indicate pronouncedly unfavorable conditions across multiple timeframes.

From an analytical perspective, today's decline reinforces the broadly unfavorable near-term market character suggested by our analysis. The inability to build upon last week's gains, despite the strong prior momentum, indicates that the underlying negative signals observed previously have not yet been negated. Confirmation of a sustainable improvement in market conditions remains elusive, supporting a cautious stance.

TOP 10 U.S. COMPANIES

Performance among the largest U.S. companies was mostly negative on Monday, reflecting the broader market pullback and specific concerns related to trade policy announcements.

Looking at individual stock performance for the day: Berkshire Hathaway Inc Class B fell sharply by -5.12%, retreating from record highs following the weekend news of Warren Buffett's intention to step down as CEO at year-end. Technology and communication stocks were also generally weaker. Netflix (not in top 10 but impacted by film tariff news) reportedly fell, potentially weighing on sentiment for streamers. Among the top 10, Amazon.com Inc declined -1.91%, Apple Inc retreated -3.15%, Tesla Inc fell -2.42%, Broadcom Inc lost -1.43%, and NVIDIA Corp slipped -0.59%. Alphabet Inc Class A managed a slight gain of +0.11%, as did Microsoft Corp (+0.20%). Meta Platforms Inc also gained +0.38%. JPMorgan Chase & Co edged higher by +0.02%.

Interpreting the underlying analytical signals, the near-term market character for most of these leading companies remained unfavorable or neutral according to our indicators. Today's generally negative price action aligns with this underlying caution. The sharp drop in Berkshire Hathaway reflects specific company news, while weakness in other large-cap names highlights sensitivity to broader market sentiment and trade policy risks.

ECONOMIC INDICATORS

Today's primary economic data point, the ISM Services PMI for April, presented a mixed message for investors and policymakers. The headline index reading of 51.6 indicated stronger-than-expected expansion in the services sector, suggesting resilience despite economic headwinds. However, components within the report raised concerns: the Prices Paid index surged, indicating mounting inflationary pressures within the sector, and commentary from respondents frequently cited uncertainty and negative impacts stemming from tariffs.

This official data provides context for our suite of economic indicators. The strong ISM activity aligns somewhat with the neutral signal for Investment Duration observed recently in our analysis, suggesting the market isn't signaling an immediate collapse. However, the rising prices component in the ISM survey could challenge the recent easing observed in our Inflation indicator signals, warranting close monitoring. The persistently weak signal from our Consumer Strength indicator remains a concern, aligning with cautious comments from some service sector respondents and weak confidence data last week. The Corporate Earnings outlook derived from market analysis continues to appear muted. Overall, the economic picture remains complex, with service sector activity holding up but facing rising cost pressures and tariff impacts, complicating the outlook ahead of the Fed meeting.

SECTOR OVERVIEW

Sector performance within the S&P 500 was broadly negative on Monday, reflecting the risk-off tone as the market's winning streak ended. Ten out of eleven sectors finished lower, with cyclical and technology-related groups generally leading the decline.

Energy (-1.81%) was the worst-performing sector, likely pressured by ongoing concerns about global demand and potentially reacting to prior session weakness in crude oil prices. Information Technology (-0.68%) also fell notably. Consumer Discretionary (-1.06%) retreated, consistent with ongoing concerns about consumer spending. Materials (-0.74%) and Financials (-0.64%) also declined. Defensive sectors offered relative, though not absolute, safety: Utilities (-0.25%), Real Estate (-0.36%), and Healthcare (-0.28%) saw smaller losses. Consumer Staples (-0.09%) finished nearly flat, showing the most resilience. The only sector managing a gain was Industrials (+0.05%).

From an analytical perspective, today's broad decline across most sectors reinforces the unfavorable or neutral near-term conditions indicated by our analysis for the majority of the market. The relative strength in defensives aligns with a cautious underlying tone. Sustained weakness across cyclical and growth sectors would further confirm the negative near-term outlook suggested by our indicators.

INTERNATIONAL MARKETS

International markets also experienced pullbacks on Monday, following the negative lead from the U.S. and reflecting shared concerns about global trade uncertainty. The U.S. Dollar strengthened slightly, rising +0.11% for the day.

Developed markets declined: European equities fell -0.49% and Japanese equities lost -0.64%. Despite recent indications of strengthening characteristics from analysis, these markets remain sensitive to global risk sentiment and trade developments emanating from the U.S.

Emerging markets were also broadly lower: Emerging Markets Asia fell -1.11%, India declined -0.76%, and Latin America lost -1.00%. Chinese equities retreated -0.04%, outperforming slightly on a relative basis but still ending lower. The broad declines underscore the global nature of concerns surrounding trade policy impacts.

OTHER ASSETS

Activity across other asset classes on Monday generally reflected a cautious, risk-off mood. Bonds saw mixed price action, most commodities were lower, while gold bucked the trend, and the dollar firmed slightly.

In fixed income, U.S. Treasury prices were mixed. Short-term Treasury prices declined slightly (-0.01%), while Intermediate Treasury prices fell -0.18%. Long-term Treasury prices bucked the trend, managing a gain of +0.04%. Broad U.S. Aggregate Bond prices decreased -0.15%. This suggests limited flight-to-safety demand despite the equity pullback.

Commodity performance was mostly negative, with one notable exception. WTI Crude Oil fell -2.56%. Base Metals gained +0.22%. Agricultural Commodities declined -0.56%. Notably, Gold prices surged +2.99%, acting as a haven asset amidst the equity market pullback and trade uncertainty. The US Dollar Index strengthened slightly, rising +0.11%. In digital assets, Bitcoin prices declined -2.83%, moving lower with other risk assets.

Join the official LINE account of "Joe’s Wall Street Pulse" now to receive the latest column updates (click here to join)