•

【Joe’s華爾街脈動】標普500指數震盪,投資者消化聯準會決策、貿易前景與財報

聯準會維持利率不變,警告風險上升;川普對中國關稅立場強硬

Joe Lu, CFA 2025年5月7日 美東時間

市場概況

美國股市週三在投資者消化美國聯準會維持利率不變的決策、持續的貿易政策不確定性以及特定公司消息的過程中,經歷了震盪的交易。正如市場普遍預期,聯邦公開市場委員會(FOMC)將基準利率維持在4.25%至4.50%的目標區間。然而,隨後的聲明以及主席鮑爾的記者會卻釋放出更為謹慎的基調,承認「經濟前景的不確定性進一步增加」,並明確指出「失業率上升和通膨上升的風險均已升高」。鮑爾直接將潛在的持續性關稅調升與經濟成長放緩、長期通膨上升以及失業率增加聯繫起來,勾勒出央行在政策權衡上所面臨的艱難局面。

在美東時間下午2點宣布後,市場反應劇烈震盪。股市最初回吐部分漲幅,隨後在盤中稍晚收復。標普500指數最終收高+0.42%。道瓊工業平均指數上漲+0.69%,部分受惠於迪士尼財報優於預期後股價的上揚。以科技股為主的那斯達克綜合指數亦上漲,漲幅為+0.40%。以羅素2000指數為代表的小型股上漲+0.33%。部分策略師認為,聯準會聲明中強調雙向風險的措辭略偏鷹派,暗示在政策不確定性下並不急於降息。摩根大通資產管理公司首席全球策略師David Kelly指出,聯準會似乎就其政策的經濟風險向政府發出了「警告」。

在原已複雜的局勢中再添變數,川普總統於聯準會公告決策前數小時重申其對中國關稅的堅定立場,表示在財政部長Bessent與中國代表計劃舉行會談之前,他不會考慮下調145%的關稅以吸引北京重回談判桌。這強化了鮑爾所認為的貿易緊張局勢是一關鍵不確定因素。儘管鮑爾堅稱,目前經濟仍處於「穩健狀態」,但對風險的日益關注表明聯準會仍高度依賴數據。市場目前正持續應對來自貨幣政策、貿易談判與即將公布的經濟數據等多方訊號交錯所帶來的混亂局勢。

重點摘要

- 主要美股指數在聯準會公告維持利率不變的決策後,經歷震盪交易,收盤漲跌互見:標普500指數 (+0.42%),道瓊工業平均指數 (+0.69%),那斯達克綜合指數 (+0.40%)。

- 美國聯準會承認經濟不確定性增加,且就業與通膨雙雙面臨風險上升,突顯貿易政策可能引發的停滯性通膨擔憂。

- 根據分析,儘管指數表現漲跌互見至小幅上揚,潛在的近期市場特性普遍仍屬不利。

- 科技類股因AI競爭消息而出現劇烈分歧;多數類股溫和上漲。公債價格上漲,殖利率則下跌。

- 川普總統重申對中國關稅的強硬立場,表示不會為了展開談判而降低關稅,使得貿易政策在聯準會決策結果出爐後,不確定性依然存在。

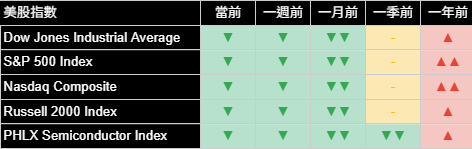

主要市場指數

在美國聯準會政策宣布後,主要市場指數週三在經歷盤中大幅波動後,收盤漲跌互見至上揚。道瓊工業平均指數 (+0.69%) 在主要基準指數中漲幅最大。標普500指數 (+0.42%) 和那斯達克綜合指數 (+0.40%) 亦收漲,而羅素2000指數 (+0.33%) 漲幅較為溫和。儘管聯準會承認風險增加,市場仍能收高,這表明即使不確定性已被強調,投資者可能從其並未明顯轉向強硬的立場中找到些許安慰。

費城半導體指數大漲+1.77%,表現遠優於整體市場和其他科技指數,可能受惠於有報導稱川普政府計劃撤銷拜登時代的部分AI晶片限制。

從分析角度來看,儘管多數指數收盤上漲,但根據我們基於近期趨勢比較的分析,潛在的近期市場特性普遍仍屬不利。今日的漲幅雖正面積極,但在我們的指標框架內,並未構成對前幾週觀察到的負面訊號的決定性逆轉。潛在市場狀況出現可持續改善仍需確認。

美國前十大公司

美國大型企業週三表現顯著分歧,反映出在聯準會決策的背景下,科技類股內部因特定消息事件而出現的巨大差異。

觀察個股當日表現:輝達 (NVIDIA Corp) 大漲+3.10%,可能受惠於有關放寬AI晶片限制的報導。亞馬遜 (Amazon.com Inc) 在其財報公布後上漲+2.00%。Meta Platforms Inc 上漲+1.62%,博通 (Broadcom Inc) 上漲+2.36%。微軟 (Microsoft Corp) 收盤近乎持平 (+0.01%)。形成鮮明對比的是Alphabet Inc A股 (Alphabet Inc Class A) 暴跌-7.26%,據報導是在蘋果服務部門主管作證提及,正為Safari瀏覽器探索其他AI搜尋合作夥伴(如OpenAI、Perplexity、Anthropic),此消息可能威脅到Google利潤豐厚的預設搜尋協議。蘋果 (Apple Inc) 本身在該消息後亦下跌-1.14%。特斯拉 (Tesla Inc) 上漲+0.32%。金融股表現好壞參半,摩根大通 (JPMorgan Chase & Co) 上漲+0.06%,而波克夏海瑟威B股 (Berkshire Hathaway Inc Class B) 上漲+1.15%。

從底層分析訊號來看,我們的分析指標表示,這些領先企業中大多數的近期市場特性仍偏向疲弱或中性,其中Alphabet今日進一步惡化。劇烈的分歧突顯了公司特定消息流的影響,特別是在整體市場環境中與AI競爭和定位相關的消息。這些個股的個別題材目前正蓋過整體指數對這些特定股票的趨勢影響。

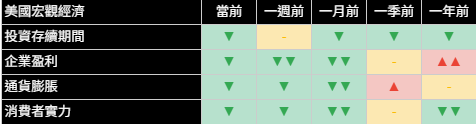

經濟指標

美國聯準會的政策聲明和主席鮑爾的記者會是今日經濟訊號的焦點。聯邦公開市場委員會維持利率不變的決定符合預期,但明確承認不確定性增加以及通膨和就業雙雙面臨風險上升,標誌著基調的重大轉變。鮑爾的評論強調了持續高關稅對經濟成長、通膨和就業的潛在負面衝擊,將當前局勢框定為具有停滯性通膨風險。

我們整套經濟指標持續反映出聯準會所指出的這些謹慎因素。分析顯示,今日投資存續期間訊號略有改善,從極為不利轉為中度不利,但仍反映出在不確定性加劇的情況下,市場偏好較短的投資期限。消費者信心訊號依然疲弱,與聯準會對就業潛在衝擊的擔憂一致。從市場分析推估出的企業獲利前景亦持續不利。當日通膨訊號保持穩定,與近期緩和趨勢一致,但仍高於能明確促使聯準會寬鬆的水平,特別是考慮到鮑爾提及的關稅因素。聯準會聲明中強調雙向風險增加,驗證了這些指標一直以來所突顯的謹慎訊號。

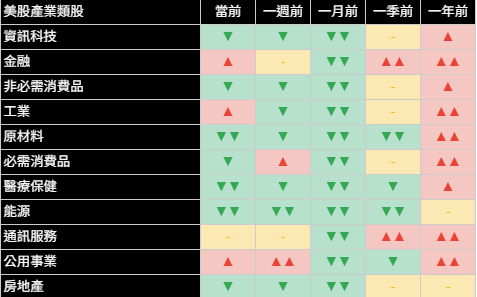

類股概況

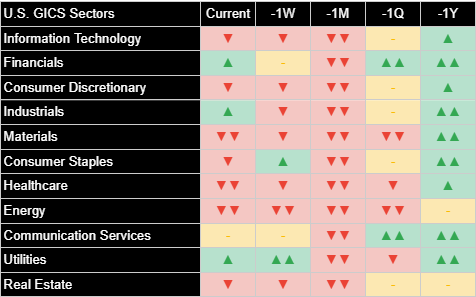

標準普爾500指數各類股週三表現大多為正,儘管漲幅普遍溫和,僅特定領域表現突出,反映出在聯準會宣布以及科技股顯著分歧後的震盪交易。

資訊科技類股 (+1.00%) 表現最佳,但這掩蓋了內部顯著的分歧,半導體股的強勁漲勢被Alphabet等主要參與者的急劇下跌所抵銷。金融類股 (+0.59%)、非必需消費品類股 (+0.78%) 和醫療保健類股 (+0.77%) 亦錄得穩健漲幅。工業類股 (+0.51%)、公用事業類股 (+0.29%)、必需消費品類股 (+0.16%) 和房地產類股 (+0.10%) 漲幅較小。通訊服務類股 (-0.18%) 微幅收低,儘管Meta有所上漲,仍受Alphabet急跌拖累。能源類股 (+0.04%) 收盤近乎持平,而原物料類股 (-0.55%) 則是表現最疲弱的類股。

從分析角度來看,儘管許多類股當日價格走勢正面,但我們分析所顯示的多數類股潛在近期狀況仍為不利或中性。科技類股的強勁表現範圍狹窄,主要由半導體股推動。類股整體缺乏廣泛、決定性的正面轉變,表明市場仍處於不確定和盤整時期。

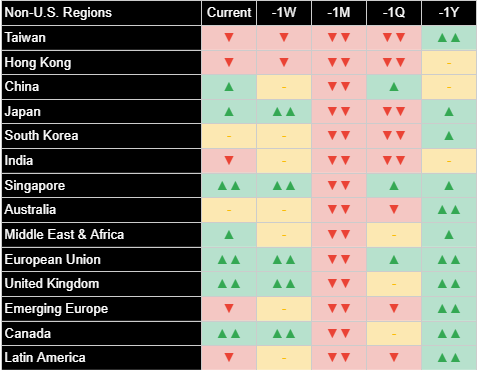

國際市場

國際市場週三表現好壞參半,全球投資者消化美國聯準會語氣謹慎的聲明以及美國持續的貿易政策評論。美元顯著走強,當日上漲+0.73%。

已開發市場表現好壞參半:歐洲股市下跌-0.31%,而日本股市則下跌-0.62%。分析持續顯示,從較長的時間區間來看,這些地區呈現出日益增強的正向特徵,但它們對聯準會訊號和美國政策走向仍然敏感。

新興市場亦呈現不同結果:新興亞洲市場下跌-1.49%,印度下跌-0.86%,拉丁美洲亦下跌-0.32%。中國股市經歷顯著下跌,跌幅達-2.34%。美元走強可能對新興市場資產構成壓力。

其他資產

週三其他資產類別的活動反映了市場消化聯準會立場、持續的貿易擔憂以及美元走強的影響。債券上漲,而多數大宗商品則回檔。

固定收益方面,在聯準會承認經濟風險增加後,美國公債價格上漲,殖利率則下跌。短期公債價格上漲+0.04%,中期公債價格上漲+0.26%,長期公債價格上漲+0.42%。整體美國綜合債券價格上漲+0.15%。對債券的需求表明投資者關注聯準會所強調的不確定性上升。

大宗商品表現大多為負,受美元走強打壓。WTI原油下跌-1.69%。黃金價格亦下跌,跌幅為-1.50%。基本金屬下跌-0.77%。農產品微幅下跌-0.04%。美元指數顯著走強,上漲+0.73%。在數位資產方面,比特幣價格上漲+1.32%。

立即加入《Joe’s 華爾街脈動》LINE@官方帳號,獲得最新專欄資訊(點此加入)

關於《Joe’s 華爾街脈動》

鉅亨網特別邀請到擁有逾 22 年美國投資圈資歷、CFA 認證的機構操盤人 Joseph Lu 擔任專欄主筆。 Joe 為台裔美國人,曾管理超過百億美元規模的基金資產,並為總資產高達數千億美元的多家頂級金融機構提供資產配置優化建議。 Joe 目前帶領著由美國頂尖大學教授與博士組成的精英團隊,透過獨家開發的 "趨勢脈動 TrendFolios® 指標",為台灣投資人深度解析全球市場脈動,提供美股市場第一手專業觀點,協助投資人掌握先機。

S&P 500 Gyrates as Investors Digest Fed Decision, Trade Outlook and Earnings

Fed Holds Rates, Warns of Rising Risks; Trump Digs In on China Tariffs

Joe Lu, CFA May 7, 2025

MARKET OVERVIEW

U.S. equity markets navigated a volatile session on Wednesday as investors processed the Federal Reserve's decision to hold interest rates steady alongside persistent trade policy uncertainties and specific company news. As widely anticipated, the Federal Open Market Committee (FOMC) maintained the benchmark federal funds rate in its target range of 4.25% to 4.50%. However, the accompanying statement and subsequent press conference from Chair Jerome Powell introduced a more cautious tone, acknowledging that "uncertainty about the economic outlook has increased further" and explicitly stating that "the risks of higher unemployment and higher inflation have risen." Powell directly linked potential sustained tariff increases to slower growth, higher long-term inflation, and increased unemployment, framing the difficult balancing act the central bank faces.

The market reaction was choppy following the 2:00 PM ET announcement. Stocks initially ceded some gains before recovering later in the session. The S&P 500 Index ultimately finished higher by +0.42%. The Dow Jones Industrial Average gained +0.69%, aided partly by a pop in Disney shares after its earnings beat. The technology-heavy Nasdaq Composite Index also rose, adding +0.40%. Small-capitalization stocks, represented by the Russell 2000 Index, gained +0.33%. Some strategists interpreted the Fed's statement highlighting two-sided risks as somewhat hawkish, implying no hurry to cut rates given the policy uncertainties. David Kelly, chief global strategist at JPMorgan Asset Management, noted the Fed seemed to be sending a "shot across the bow to the administration" regarding the economic risks of its policies.

Adding to the complex backdrop, President Trump reiterated his firm stance on China tariffs just hours before the Fed decision, stating he would not consider lowering the 145% duties to entice Beijing to the negotiating table ahead of planned talks between Treasury Secretary Bessent and his Chinese counterpart. This reinforced the trade tensions that Powell acknowledged as a key uncertainty. While Powell maintained the economy remains "in solid shape" currently, the increased focus on risks suggests the Fed remains firmly data-dependent. The market continues to grapple with these conflicting signals from monetary policy, trade negotiations, and incoming economic data.

EXECUTIVE SUMMARY

- Major U.S. indices finished mixed after a choppy session digesting the Fed's decision to hold rates steady: S&P 500 Index (+0.42%), Dow Jones Industrial Average (+0.69%), Nasdaq Composite Index (+0.40%).

- The Federal Reserve acknowledged increased economic uncertainty and rising risks to both employment and inflation, highlighting potential stagflation concerns stemming from trade policy.

- Underlying near-term market character remained broadly unfavorable according to analysis, despite the mixed-to-positive index performance.

- Technology sector showed sharp divergences related to AI competition news; most sectors gained modestly. Treasury prices rose as yields fell.

- President Trump reiterated a hard line on China tariffs, stating he wouldn't lower them to start talks, maintaining trade policy uncertainty despite the Fed outcome.

BROAD MARKET INDICES

Broad market indices finished mixed to higher on Wednesday after navigating significant intraday volatility surrounding the Federal Reserve's policy announcement. The Dow Jones Industrial Average (+0.69%) posted the strongest gain among the major benchmarks. The S&P 500 Index (+0.42%) and the Nasdaq Composite Index (+0.40%) also finished in positive territory, while the Russell 2000 Index (+0.33%) saw a more modest advance. The market's ability to close higher despite the Fed acknowledging increased risks suggests investors may have found some reassurance in the lack of an overtly hawkish shift, even as uncertainty was highlighted.

The PHLX Semiconductor Index surged +1.77%, strongly outperforming the broader market and other tech indices, possibly boosted by reports suggesting the Trump administration plans to rescind some Biden-era AI chip restrictions.

From an analytical perspective, despite the positive closing prices for most indices, the underlying near-term market character remained predominantly unfavorable according to our analysis based on recent trend comparisons. Today's gains, while welcome, did not constitute a decisive reversal of the negative signals observed over the preceding weeks within our indicator framework. Confirmation of a sustainable improvement in underlying market conditions is still required.

TOP 10 U.S. COMPANIES

Performance among the largest U.S. companies was notably mixed on Wednesday, reflecting significant divergence within the technology sector following specific news events, set against the backdrop of the Fed decision.

Looking at individual stock performance for the day: NVIDIA Corp surged +3.10%, potentially benefiting from reports about easing AI chip restrictions. Amazon.com Inc gained +2.00% following its earnings report. Meta Platforms Inc rose +1.62%, and Broadcom Inc advanced +2.36%. Microsoft Corp finished nearly flat (+0.01%). In stark contrast, Alphabet Inc Class A plummeted -7.26%, reportedly after Apple's services chief testified about exploring alternative AI search partners (like OpenAI, Perplexity, Anthropic) for Safari, potentially threatening Google's lucrative default search deal. Apple Inc itself fell -1.14% following that news. Tesla Inc gained +0.32%. Financials were mixed, with JPMorgan Chase & Co rising +0.06%, while Berkshire Hathaway Inc Class B gained +1.15%.

Interpreting the underlying analytical signals, the near-term market character for most of these leading companies remained unfavorable or neutral according to our indicators, with Alphabet deteriorating further today. The sharp divergences highlight the impact of company-specific news flow, particularly related to AI competition and positioning, within the broader market environment. These individual stories are currently overshadowing broader index trends for these specific names.

ECONOMIC INDICATORS

The Federal Reserve's policy statement and Chair Powell's press conference were the central focus for economic signals today. The FOMC's decision to hold rates steady was expected, but the explicit acknowledgment of increased uncertainty and rising risks to both inflation and employment marked a significant tonal shift. Powell's commentary underscored the potential negative impacts of sustained high tariffs on growth, inflation, and jobs, framing the current situation as posing stagflationary risks.

Our suite of economic indicators continues to reflect elements of this caution identified by the Fed. Analysis indicated a slight improvement in the Investment Duration signal today, moving from pronouncedly unfavorable to moderately unfavorable, though still reflecting a preference for shorter horizons consistent with heightened uncertainty. The Consumer Strength signal remained weak, aligning with the Fed's concern about potential impacts on employment. The outlook for Corporate Earnings derived from market analysis also remained unfavorable. Inflation signals remained stable on the day, consistent with recent easing but still above levels that would clearly prompt Fed easing, especially given the tariff overlay mentioned by Powell. The Fed's statement focusing on increased two-sided risks validates the cautious signals these indicators have been highlighting.

SECTOR OVERVIEW

Sector performance within the S&P 500 was mostly positive on Wednesday, though gains were generally modest outside of specific pockets of strength, reflecting the choppy trading following the Fed's announcement and significant tech divergence.

Information Technology (+1.00%) was the top performer, but this masked significant internal divergence, with strong gains in semiconductors offset by sharp losses in major players like Alphabet. Financials (+0.59%), Consumer Discretionary (+0.78%), and Healthcare (+0.77%) also posted solid advances. Industrials (+0.51%), Utilities (+0.29%), Consumer Staples (+0.16%), and Real Estate (+0.10%) saw smaller gains. Communication Services (-0.18%) finished slightly lower, dragged down by Alphabet's sharp decline despite gains in Meta. Energy (+0.04%) was nearly flat, while Materials (-0.55%) was the weakest performing sector.

From an analytical perspective, the underlying near-term conditions indicated by our analysis remained unfavorable or neutral for most sectors, despite the positive daily price action for many. The strong performance in Technology was narrow, driven significantly by semiconductors. The lack of broad, decisive positive shifts across the sector landscape suggests the market remains in a period of uncertainty and consolidation.

INTERNATIONAL MARKETS

International markets displayed mixed performance on Wednesday as investors globally digested the U.S. Federal Reserve's cautiously toned statement and ongoing trade policy commentary from the U.S. The U.S. Dollar strengthened significantly, rising +0.73% for the day.

Developed markets were mixed: European equities fell -0.31% while Japanese equities declined -0.62%. Analysis continues to indicate strengthening positive characteristics for these regions over longer horizons, but they remain sensitive to Fed signals and U.S. policy direction.

Emerging markets also showed varied results: Emerging Markets Asia fell -1.49%, India declined -0.86%, and Latin America also lost -0.32%. Chinese equities experienced a notable decline, falling -2.34%. The stronger U.S. dollar likely acted as a headwind for emerging market assets.

OTHER ASSETS

Activity across other asset classes on Wednesday reflected the market digesting the Fed's stance, ongoing trade concerns, and a stronger U.S. dollar. Bonds gained, while most commodities retreated.

In fixed income, U.S. Treasury prices registered gains as yields fell following the Fed's acknowledgment of increased economic risks. Short-term Treasury prices rose +0.04%, Intermediate Treasury prices gained +0.26%, and Long-term Treasury prices advanced +0.42%. Broad U.S. Aggregate Bond prices increased +0.15%. The demand for bonds suggests investors focused on the rising uncertainty highlighted by the Fed.

Commodity performance was mostly negative, pressured by the stronger dollar. WTI Crude Oil fell -1.69%. Gold prices also declined, losing -1.50%. Base Metals fell -0.77%. Agricultural Commodities managed a slight loss of -0.04%. The US Dollar Index strengthened notably, rising +0.73%. In digital assets, Bitcoin prices gained +1.32%.

Join the official LINE account of "Joe’s Wall Street Pulse" now to receive the latest column updates (click here to join)